After years of low prevailing levels of inflation, investors are now starting to consider the impact that potentially higher inflation may have on their portfolios. The risk of inflation is real, for at least four main reasons:

- The economic impact of the pandemic has led central banks around the globe to cut interest rates and buy bonds to inject money into the economy and support growth.

- The substantial fiscal stimulus response by governments has rapidly increased the amount of money in the system, stoking demand.

- The rapid development of multiple vaccines and a large global vaccination program means economic activity is expected to rise quickly through the summer and into the fall.

- Central banks have stated they intend to allow inflation to run slightly hotter than usual before raising interest rates.

Together, these conditions could allow for moderate levels of inflation to take root.

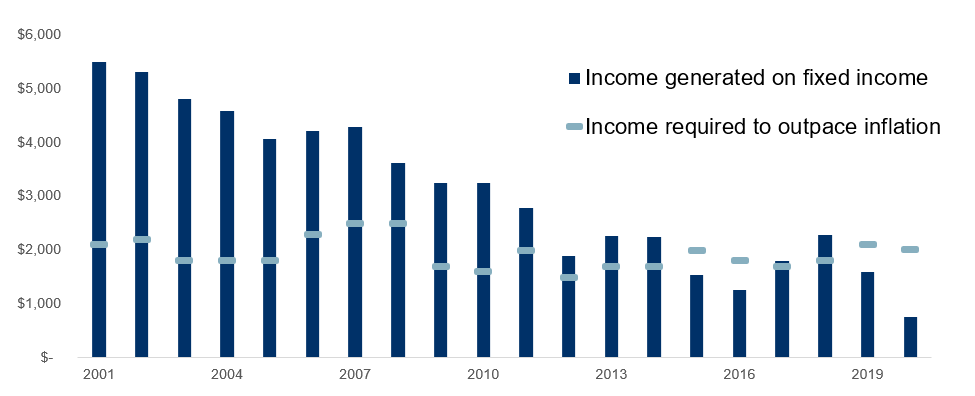

While far from a certainty, a future of higher inflation has important implications for your portfolio. Put simply, inflation reduces purchasing power as it erodes the value of cash over time. Things cost more, so you need more money to buy the same things. For investors, the question is whether the return on their investments outpaces the rate at which their purchasing power is declining. It’s even more important when interest rates are low. As the chart below shows, declining interest rates have meant that investors holding government bonds have seen their purchasing power reduced even in an environment with low inflation.

Income generated by fixed income vs. inflation

Based on $100,000

Data as of December 31, 2020. Source: Bloomberg, Bank of Canada, RBC GAM. Bond income based on annual yields for Government of Canada 10-year bonds. Inflation based on median core Consumer Price Index (CPI).

Preparing your portfolio to withstand moderate levels of inflation can be thought of from three different viewpoints: that of a fixed income investor, an equity investor, and from a balanced portfolio perspective.

The effect of inflation on bonds and other fixed income

Broadly speaking, the fixed income market is largely driven by interest rate expectations. Inflation impacts the bond market in two ways:

- It drives up yields. A yield is the annualized return you receive on a bond if you hold it until its maturity date. When inflation rises, interest rates also tend to rise. This in turn causes bond prices to drop. If you wanted to sell your bond before the maturity date, you would get a lower price than you paid.

- It erodes the purchasing power of the payments you receive from fixed interest investments. It does the same thing to the dollars you have invested and will receive back when you sell the investments or they mature.

How to reduce inflation’s impact

- Shorter-term bonds. When you shorten the time between when you purchase the bond and when it matures, you reduce your exposure to changing interest rates. When inflation expectations rise, so do bond yields. This causes prices for bonds to move lower. Investing in shorter term bonds helps protect you from the negative impacts of rising inflation expectations. This can lead to a smoother investment experience.

- Higher-risk bonds. When you invest in bonds, there’s a graduated scale of risk. Bonds from governments with a good borrowing history are often rated “risk-free.” You are almost certain to be repaid. But you will likely receive less interest (the bond yield) than other bonds that come with higher risk – for example, bonds from governments or companies with higher debt levels or more volatile revenues. Buying higher-risk bonds boosts your yield and helps you stay ahead of inflation, though they do come with a higher risk of default than “risk-free” bonds.

- Global bonds. Inflation may be more prevalent in some countries than others. For example, Japan’s aging population and low immigration levels are likely to keep inflation in check. Diversifying your bond exposure outside of North America can help lessen the impact that rising local interest rates would have on your portfolio, though currency considerations should be taken into account.

- Flexible yields. Some fixed income products provide more flexibility, changing their yield as interest rates change. Examples include floating rate notes and rate reset preferred shares. However, active management is important to take advantage of the rising rate environment. The sensitivity to growth also needs to be closely managed.

- Alternative bond strategies. Some funds have the flexibility to adjust the portfolio to protect it, or even benefit, from rising rates. The returns on these funds are primarily driven by the decisions of the investment manager instead of broad market returns. The timing and level of returns for alternate bond strategies can differ from other bond funds. Adding this different source of returns to your portfolio can help smooth out the overall performance, improving risk-adjusted returns.

- Real return bonds (RRBs). RRBs provide a “real” yield plus inflation. They are useful tools for investors concerned about future inflation. However, these products typically have a longer time period to maturity. This means they will be more volatile and sensitive to changes in real yields. If real yields rise, the price of the bonds will fall. This price decline could potentially be more than the income you’re receiving from these bonds in a given year. Investors thus need to be cautious when investing in RRBs.

The effect of inflation on stocks and other equities

As compared to fixed income, equities tend to protect investors better against inflation. This is because, in theory, companies should be able to grow their earnings and revenues at a rate that matches or exceeds inflation. Yet higher inflation can discourage corporate investment which in turn can lead to lower overall returns.

Inflation’s impact on valuations is also an important consideration. In the past, higher inflation has been associated with lower price-to-earnings multiples (P/Es). For example, in the 1970s inflation was accelerating, and as P/Es compressed, stocks came under pressure despite continued growth in earnings. This could be an additional headwind for stocks, particularly for companies with stretched valuations. However, the impact could potentially be mitigated if interest rates are kept lower for longer under the Fed’s new average inflation targeting framework.

Specific areas of the equity market that tend to fare better during times of inflation include:

- Companies with ties to commodities and natural resources, including gold. When demand for goods increases the demand for commodities rises, which leads commodity prices to increase alongside of accelerating inflation. Companies that generate revenues that are tied to the price of commodities see their revenues rise in kind, offering a degree of protection against rising inflation.

- Fixed investments such as property and real estate. Real assets generally store value, meaning that their prices tends to rise with inflation.

- Companies that generate healthy levels of cash flow. In general, businesses that generate rather than consume cash would largely fare better during inflationary environments.

- Businesses that are scalable and able to raise prices without hurting demand would typically see their earnings increase alongside of inflation.

Conclusion

Within the context of a balanced portfolio, protection against inflation tends to lead investors to add more equities at the expense of fixed income. In theory, equities offer more upside potential and have historically demonstrated an ability to generate returns that exceed inflation. Yet equities can also lead to greater volatility – which can in turn make it harder for an investor to stick with their plan.

For this reason, fixed income can still play an important role within a diversified balanced portfolio. Used well, it can help create a smoother investment experience. The key is to choose these investments carefully, with deliberate strategies to address inflation.

One this is clear: rising inflation adds another layer to the complexities of portfolio construction. It’s essential to consider the benefits and risks from all angles.

Get the latest insights from RBC Global Asset Management.