Climate change is an unavoidable issue for governments, corporates and consumers alike, as the implications of rising temperatures and pollution levels have become increasingly apparent. In light of the current COVID-19 pandemic there are now two schools of thought for the trajectory of climate action. One is that the pandemic could lead to fundamental changes in human behaviour which may act as a tailwind for the climate change theme; the second is that the shock to the global economy coupled with lower oil prices could result in policy measures being directed elsewhere resulting in the cost trajectories for renewables and electric vehicles becoming less favourable.

Overall, while in the short term there could be a delay to climate action, we still believe that the long-term drivers are very much intact in emerging markets (EM) and that the pandemic could heighten government awareness on long-term risks. Furthermore, the pandemic has paved the way for a fundamental change in human behaviour which could have a permanent impact on the future of food production and transport emissions.

What are the key drivers behind the climate change theme?

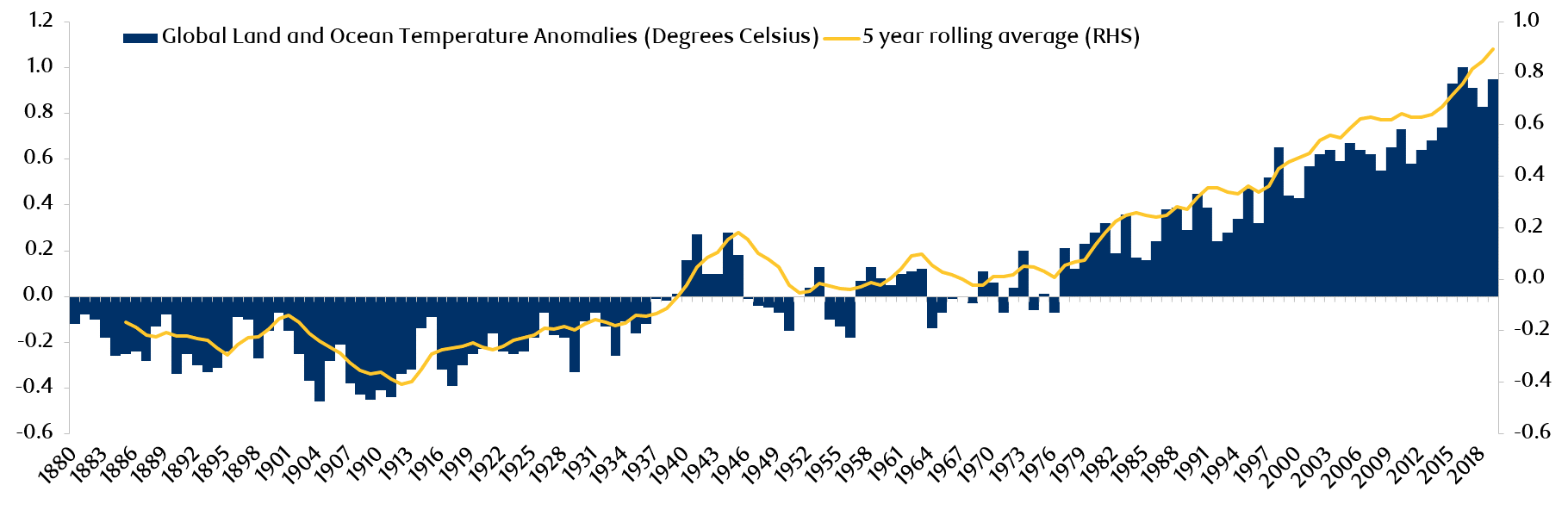

Extreme weather events are intensifying worldwide: In the U.S., for instance, 40% of cities were affected by some form of extreme weather event in 2018, more than double the number in any year during the 20th century.1 The Australian wildfires of late 2019 also highlighted the impact that extreme weather can have on habitats. Rising temperatures are the key reason for this. As illustrated in Exhibit 1, the global average temperature continues to rise, with 2019 marking one of the hottest years since records began; this is causing polar ice caps to melt and sea levels to rise. Temperature changes are also leading to abnormal patterns of precipitation, causing dry regions to become drier and wet regions to become wetter. As a result, the risk of floods has increased in urban areas, as has the number of people living in water-stressed areas. These risks highlight the importance of rethinking climate change adaptation; the world is already playing catch-up by trying to mitigate rising temperature changes by cutting CO2 emissions.

Exhibit 1: Global average temperatures have been rising

Source: NOAA National Centers for Environmental information, Climate at a Glance: Global Time Series, published May 2020. Data from 1880- December 2019. Data retrieved on May 13, 2020.

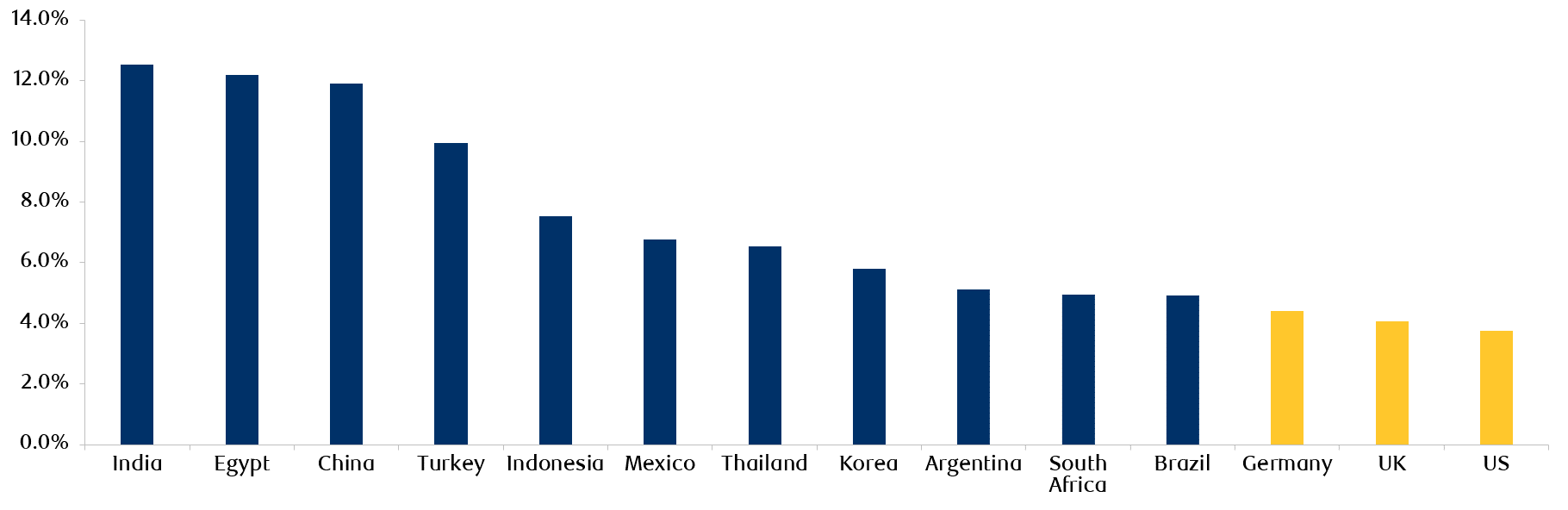

The health impacts of extreme weather events are becoming more apparent: The World Health Organization (WHO) suggests that nine out of ten people in the world breathe air containing high levels of pollution and that air pollution alone is responsible for around 7 million deaths worldwide each year.2 As illustrated in Exhibit 2, the number of deaths caused by air pollution is highest in EM. Similarly, mortality linked to climate change is projected to be higher in emerging and developing economies by 2100.3

Exhibit 2: Number of deaths from air pollution, 2017

Source: IHME (Institute for Health Metrics and Evaluation), Global Burden of Disease. Data as at December, 2018.

Heightened public awareness and activism: The climate protests that took place all over the world in 2019 were a result of heightened public awareness and growing frustration over the lack of urgency shown by governments and businesses. There has also been a rise in trends like veganism, the anti-plastic movement, flight shaming and other climate-related activism.

Demographics is an important driver, particularly in EM: The Millennial and Generation Z groups, defined as those born between 1980 and 1995 and 1996 and 2010 respectively, together make up a significant proportion of the global population: in EM alone, they account for around 46% of the population.4 The Deloitte Global Millennial Survey 2019 found that both Millennials and Gen Z identified climate change as the biggest challenge currently facing society.

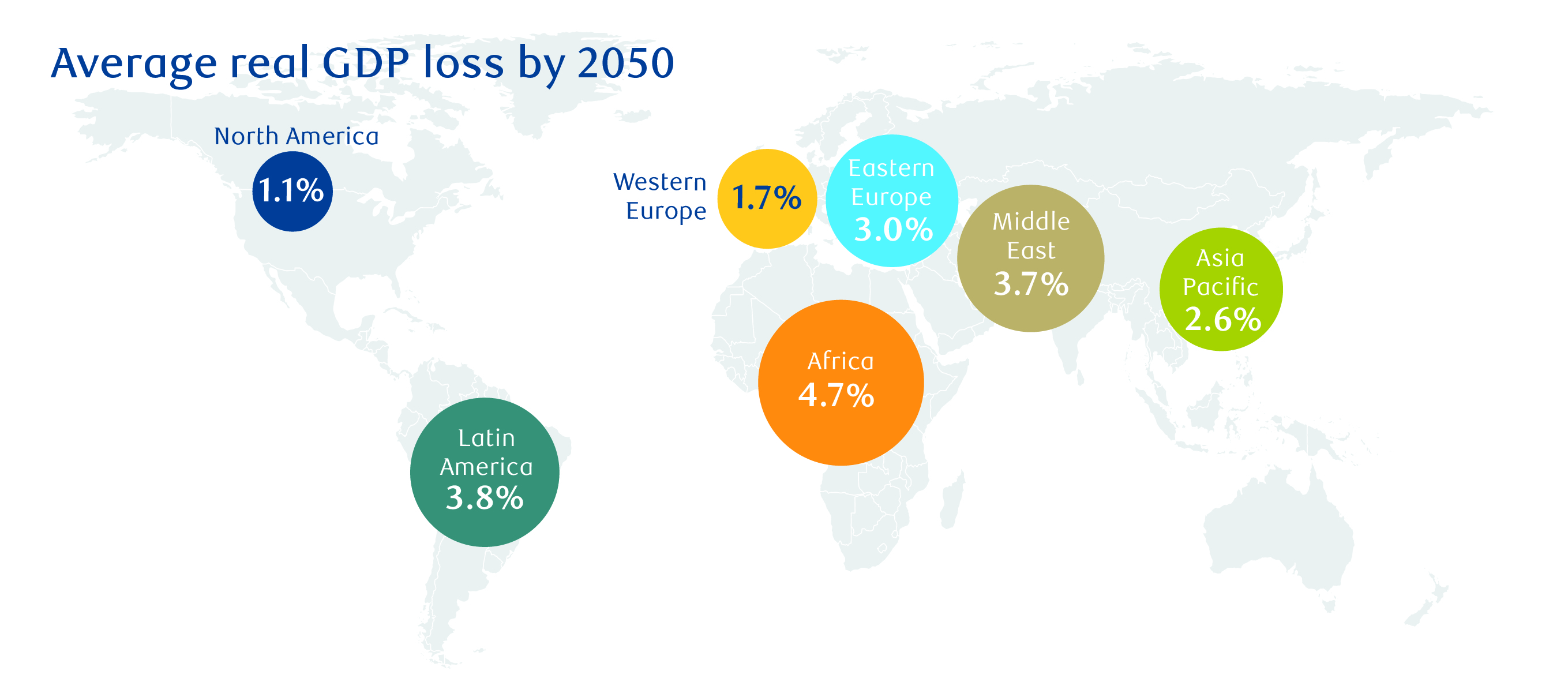

Significant financial implications, concentrated in EM: According to Moody’s, the cost of climate change to the global economy could range from US$54tn to US$69tn by 2100 if global temperatures exceed the target set by the United Nations’ Intergovernmental Panel on Climate Change (IPCC).5 Failure to act on climate issues will have negative economic consequences everywhere, but EM are projected to be the most impacted with Africa, Asia-Pacific, the Middle East and Latin America expected to suffer larger losses in real GDP terms compared to Western Europe and North America (Exhibit 3).

Exhibit 3: Estimated economic impact of climate change by 2050 in terms of real GDP loss

Source: Economist Intelligence Unit. Data as at November, 2019.

Corporates are increasingly pushing the agenda on climate change: Many companies are setting ambitious long-term goals to become carbon neutral and mitigate climate change-related risks. There is also significant pressure on corporates to limit activities considered to be ‘climate unfriendly’. This is not driven just by prudential regulations (for financial institutions), but also by regulatory reporting requirements (such as the Task Force on Climate-related Financial Disclosures) and increasingly climate-conscious stakeholders. We believe the corporate response is important as it can have a more significant impact. Businesses are able to use their financial firepower to act decisively to invest in climate-related projects without the constraints of government bureaucracy.

Technology is an important enabler of the climate change theme: As a result of technological advancement, costs are declining for renewable energy (solar and wind power) and lithium batteries used in electric vehicles which is making climate-related technologies more accessible. New technological innovations are also helping households and businesses to improve energy efficiency. For example, smart city devices such as sensors and smart meters are helping cities to reduce traffic congestion and optimize energy and water use, while laboratory-produced meat and plant-based meat alternatives are also making climate mitigation possible. Collectively these technologies will be crucial if the UN IPCC’s climate targets for 2050 are to be achieved.

Governments around the world are responding to increased public concern about the environment: 195 countries have already signed the Paris Climate Agreement and 187 have ratified it. The U.S. is a notable exception, however, announcing in June 2017 that it was pulling out of the Paris Agreement. In addition, and despite rising public pressure, the Brazilian government plans to reduce the size of the Amazon rainforest for infrastructure and farming, a move that signals a lack of commitment to fighting climate change. We believe these two examples represent short-term deviations owing to the political cycle, however, and in the longer term we believe that national climate change policies will become more stringent. This is reflected by the World Economic Forum which over the past three years has consistently identified three of the top five global risks as environmental, compared to zero back in 2009.6

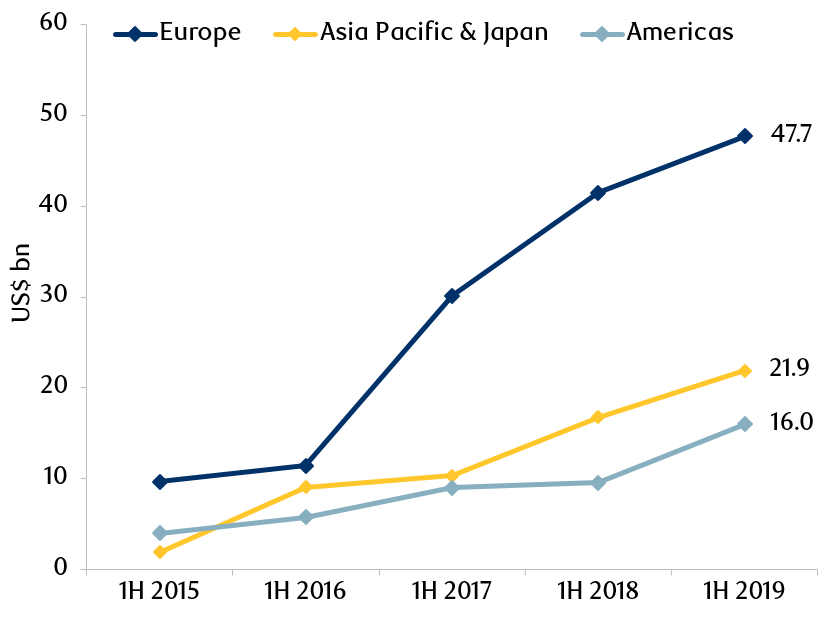

Climate and sustainable financing has increased significantly over the last decade: The majority of financing has so far been directed at the most carbon-intensive segments such as energy, construction and transport. Since 2015 private financing has accounted for over half of all climate financing (money from both public and private sources which is used to fight against the negative impacts of climate change), with the remainder coming from government funding.7 Green bonds, a type of debt instrument, have grown in popularity recently to account for the majority of all climate funding. Currently, Europe is the leading issuer of green bonds but Asia Pacific is catching up, and China is also emerging as a key player. (Exhibit 4)

Exhibit 4: Europe is the leading issuer of green bonds, but Asia is catching up

Source: Tracking the growth of green bonds, Refinitiv. Data as at July 24, 2019.

The climate change theme in EM

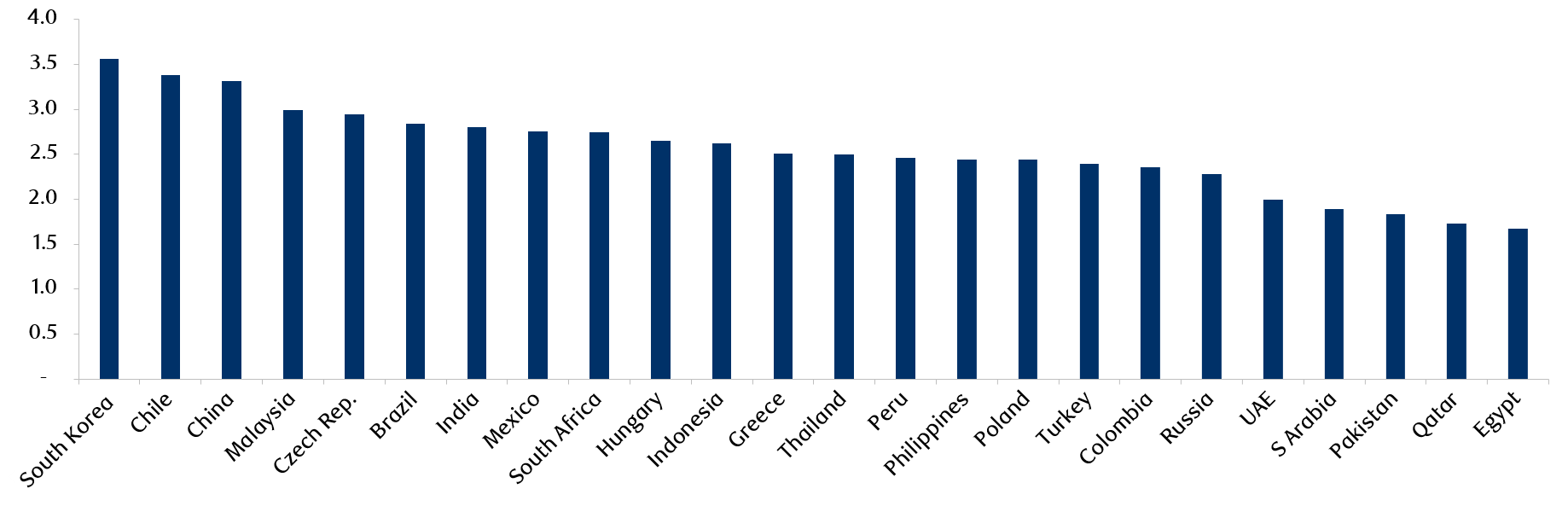

Because EM are expected to be impacted disproportionately by climate change, we think it is important to identify which countries face the biggest risks and which are the best prepared. In order to do this, we developed a country scorecard to evaluate a broad range of data across 24 EM countries, looking at both risks and preparedness. Our assessment was then combined into one composite index score for each country. Additional details on our scorecard methodology can be found in the footnotes. Exhibit 5 summarizes our results.8

Overall, South Korea, Chile, and China are the highest ranked countries in our scorecard, however breaking down the two main components of the scorecard - risks and preparedness - separately, our key findings are as follows:

- Low risks and well prepared: South Korea, Chile, China, and Malaysia.

- Higher risks and relatively well prepared: India, Czech Republic, South Africa, Thailand, and the Philippines.

- High risks and poorly prepared: Saudi Arabia, Qatar, Pakistan, and Russia.

Exhibit 5: Scorecard results (score and rankings – sorted in descending order)

Source: RBC Global Asset Management, EM Equities. Data as at March, 2020.

The impact of COVID-19 on climate change

One of the few positives to come out of the COVID-19 pandemic has been the immediate impact on greenhouse gas (GHG) emissions. Nationwide lockdowns have led to a reduction in harmful emissions with the UN reporting a drop of nearly 6% in global CO2 emissions while levels of Nitrogen Dioxide (NO2), a pollutant linked to vehicle emissions, have fallen below the 2017-2019 average. NASA satellite images have shown a dramatic decline in pollution over China, with NO2 levels 10%-30% lower than seasonal averages.

However, the question now is: will we revert to historic norms after the pandemic, or will it bring about some long-lasting changes? We highlight some of the potential outcomes related to the climate change theme below.

The positive outcomes

A fundamental change in human behaviour: Global emissions will undoubtedly recover when lockdown measures start to ease, but will we go back to business-as-usual or will there be fundamental changes to the way we live? A return to business-as-usual seems the most likely outcome, however studies have shown that times of crisis can have lasting effects too. In some ways the pandemic has induced habits that are beneficial for the climate, such as travelling less, working from home, and reducing food waste. If these habits are sustained, this could lead to a world-wide decline in emissions from sectors such as transport and food production. These two sectors account for around 40% of global GHG emissions.9

The option of substitution: Already we have seen air travel fall dramatically as a result of the pandemic. It has highlighted the possibility of substituting business travel with, for example, video conferencing and webinars. We think there could be a dramatic decline in business travel globally as technology and work-from-home services develop, and employees and businesses realize the advantages of using them.

The pandemic has also increased demand for contactless services to reduce human-to-human contact. E-commerce companies, for instance, have seen a sudden spike in demand as consumers have preferred to stay at home and have goods delivered. Although the key beneficiaries during the pandemic have been retailers of consumer staples and essential items, this trend could spill over into discretionary products once the health risks have eased.

Future of food: All available evidence suggests that the coronavirus that causes COVID-19 has a zoonotic source and concerns about these diseases, which spread from animals to humans either via meat consumption or the domestication of animals, could catalyse the growth of meat alternatives such as lab-grown and plant-based meat.10 Livestock alone accounts for around 15% of global GHG emissions.11 Disruptions to global food supply chains during the pandemic could also accelerate technology related to farming and agriculture. New farming methods, such as vertical farming, are capable of producing 25x the yield of conventional outdoor farming and also use less water, land - and produce fewer emissions.12

Increased focus on science: Interestingly, the pandemic has brought science to the forefront of mainstream media, highlighting that countries that do not heed scientific advice and prepare for future threats are at far greater risk than those that do. Thus, the pandemic could act as an eye-opener, prompting a more aggressive and co-ordinated global effort to tackle climate change.

The potential challenges

Government support remains mixed: There has been mixed support for low carbon ambitions during the pandemic. There is a fear that governments may use the pandemic as an excuse to backtrack on some of their commitments, however in EM there have been encouraging signs of a continued focus on decarbonization. South Korea recently announced its ambition for the ‘Green New Deal’ to reach net zero emissions by 2050. Furthermore, despite ongoing economic pressure, China has not revised its three-year pollution targets.

Impact of fiscal response: Globally, governments have pledged over US$8tn in fiscal support to fight the pandemic and revive ailing economies.13 One concern is that the stimulus will be directed towards highly polluting industries such as coal which could derail decarbonization efforts. While this may be the case in the near term, we still believe that any fiscal response does provide an opportunity to deploy capital towards energy efficiency. In China, for example, new energy, energy efficiency and environmental economies have all been acknowledged by the government as strategic industries.

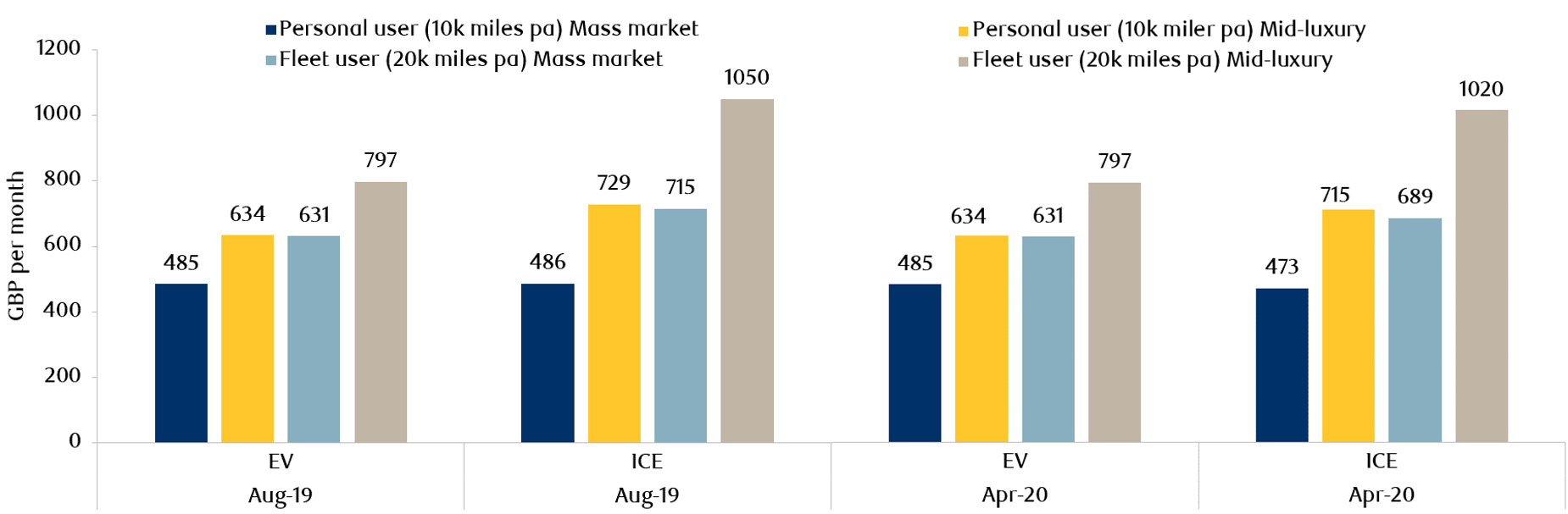

Impact of lower oil prices: In the short term decarbonization efforts could be disrupted if fossil fuels become cheaper for energy production and transportation. This could put pressure on renewable energy producers and dampen demand for electric vehicles. However, even with the lower fossil fuel prices, on average renewables are still slightly cheaper than fossil fuel power, while the cost-parity pathway for electric vehicles is still broadly intact (Exhibit 6). Furthermore, we believe that with oil prices at historic lows, there is an opportunity for governments to reduce subsidies for fossil fuel consumption – which total nearly US$400bn - since nearly half are intended to make oil products cheaper. Instead, these subsidies could be invested in the renewable energy sector to further encourage decarbonization efforts.14

Exhibit 6: Cost of owning an electric vehicle is still cheaper than an internal combustion engine, despite the recent decline in oil prices

Source: BofA Global Research, ICE = Internal Combustion Engine, EV = Electric Vehicles, Mass market are Nissan Leaf (EV) and Ford Focus (ICE), Mid-Luxury are Tesla Model 3 (EV) and BMW 3 Series (ICE). Data taken from a UK sample. Data as at May, 2020.

Watch the latest Future of Emerging Market webinar to learn more about climate change and food production trends in emerging markets.