It recently struck me that I spend a strangely large amount of my time haunting golf courses for someone who never actually fits in a round. Am I a masochist? Not at all. It just so happens that clubhouses make excellent venues for client presentations. In fact, my distance from the sport is probably for the best given that my trophy case contains a “Most Honest Golfer” award from one of the two rounds I’ve ever played.

My most recent trip to the links was unusual in that, although it was only early November, snow already blanketed the ground. While the early arrival of winter is not in itself welcome – even less so by golfers, one imagines – the contrast of the white ground and the brightly coloured leaves that still clung to branches was a rare sight and truly spectacular.

Economic Compass:

- Our latest Economic Compass is now available online: A primer on low and negative interest rates.

How much slack?

- Economists spend a disproportionate amount of time contemplating the amount of economic slack remaining in economies. “Slack” is another word for the size of the output gap – how far an economy is from its full, sustainable potential.

- A negative output gap means an economy is performing below its full potential, while a positive output gap means an economy is outperforming its full potential. If the latter situation sounds impossible, you’re nearly right – it is something that can only be sustained for a brief period of time before the economy bubbles over and recession results, sending the economy back below its potential.

- The amount of economic slack matters for a variety of reasons. It helps to determine how much remaining room an economy has for rapid growth, how much space policymakers have to deliver stimulus, and – crucially – how far along the business cycle an economy is.

- Unfortunately, output gaps cannot be directly observed. Instead they must be inferred by looking at things like unemployment rates and capacity utilization rates, and/or by identifying deviations from trend growth rates that are taken to represent overheating/underheating.

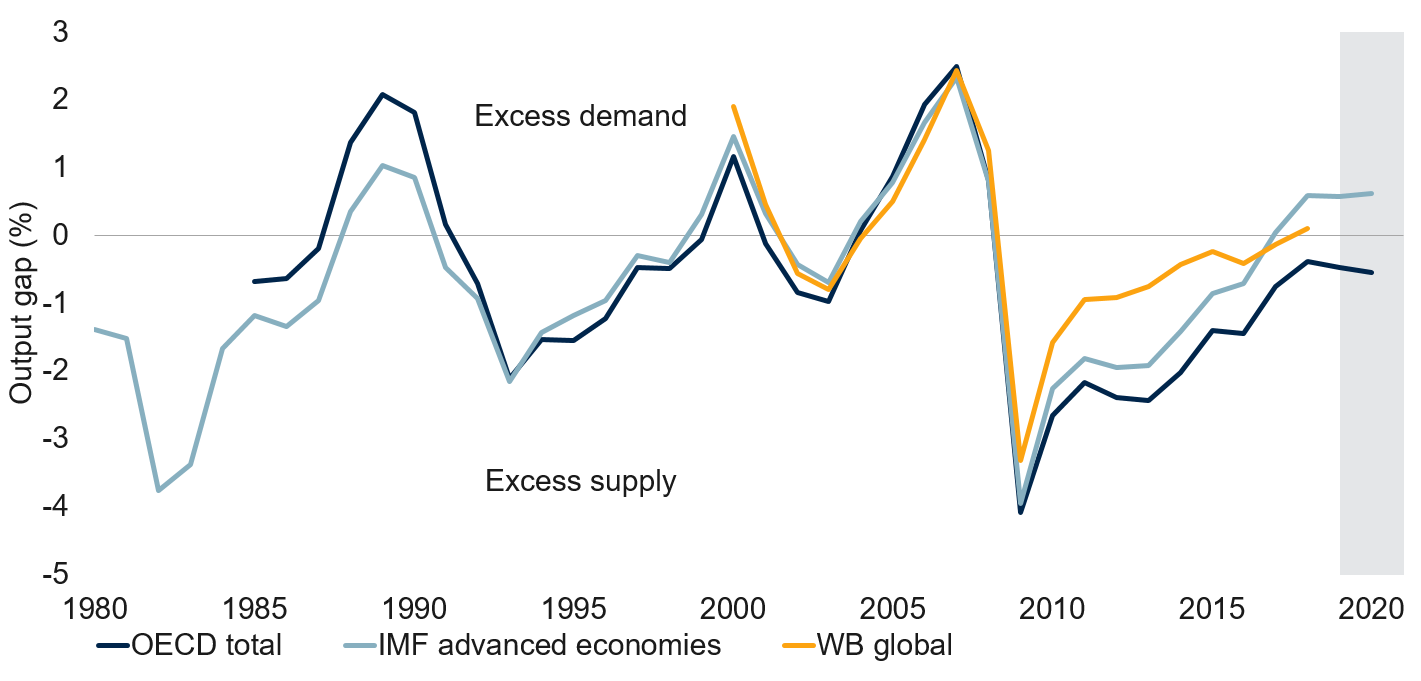

- Three institutions attempt to calculate a global output gap: the World Bank, the IMF and the OECD. In truth, only the World Bank really tallies a truly global output gap. The other two focus mostly on developed countries. This is not out of laziness – it is very hard to calculate the amount of economic slack in an emerging economy. The central complications are the large size of the (largely unmeasured) informal economy and, relatedly, the enormous latent slack remaining in countries that have not yet comprehensively urbanized. Unfortunately, the World Bank measure is staler than the rest, and also lacks a long history. As such, we rely on all three given their relative strengths (see first Exhibit).

-

Global economy is now running above potential

Note: Measured as actual GDP minus potential GDP as percentage of potential GDP. Shaded area represents IMF (Oct 2019) and OECD (May 2019) forecast. Source: IMF, OECD, World Bank, Haver Analytics, RBC GAM

- One measure claims the global economy is still moderately below its potential, another argues it is moderately above, and the final indicator says it is a hair above its potential.

- Collectively, these argue that the global economy is operating in the vicinity of its full potential, or perhaps slightly beyond.

- We now turn to the U.S., which has historically acted as something of an economic bellwether, and has also served as ground zero for many global recessions.

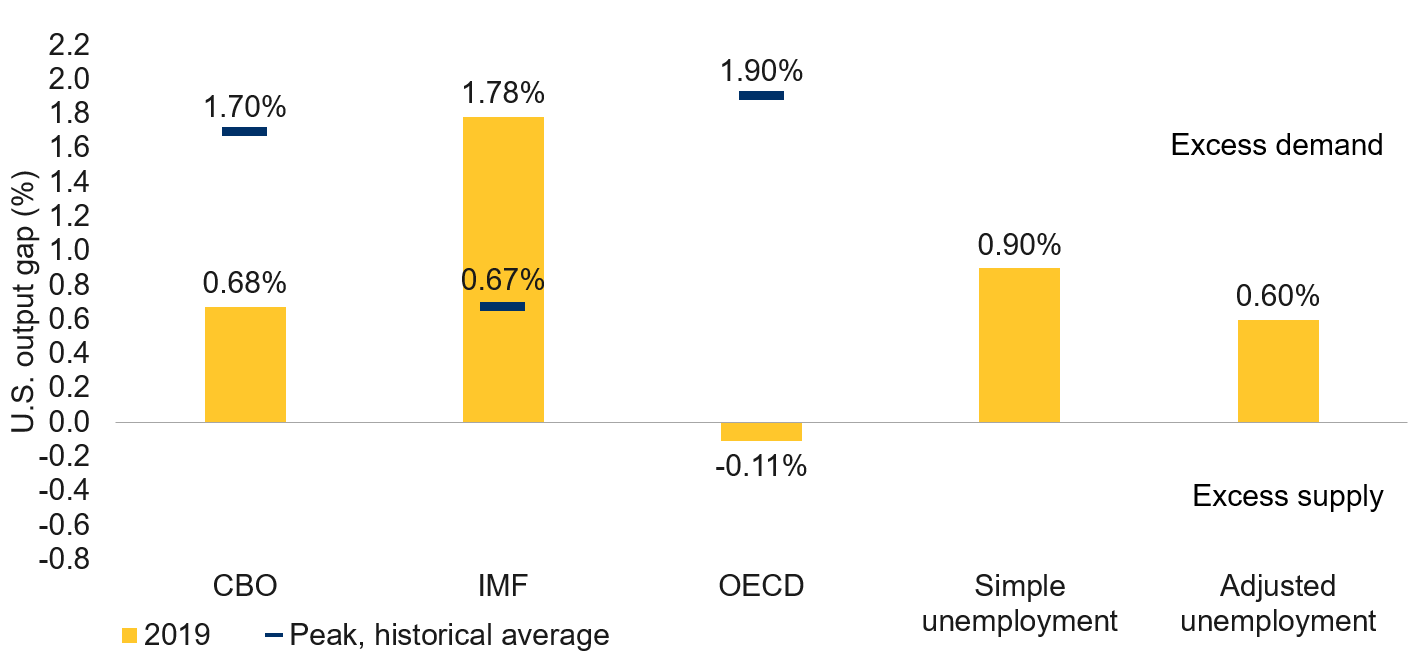

- The U.S. economy is arguably running hotter than the global economy: of the three primary estimates (from the IMF, the OECD and the Congressional Budget Office), two are significantly above potential and one is very slightly below. Collectively, these average +0.8ppt – an economy that is operating palpably past its sustainable potential (see next chart).

-

U.S. output gap – historical peak vs. now

Note: Historical average of peak output gap during each expansion estimated based on CBO data from 1950, IMF data from 1980, and OECD data from 1991. RBC GAM estimates of output gaps based on Okun's law using reported acutal and demographics adjusted unemployment. Source: CBO, IMF, OECD, Macrobond, RBC GAM

- But economies don’t usually collapse the instant they reach their potential. Instead, they have historically peaked at an average reading of +1.4ppt. This argues there is a bit of life left in the U.S. economy, even though it is already technically overheating.

- However, that’s not the final word on the subject, for two reasons:

- There are competing arguments regarding whether these output gap measures are biased to the upside versus the downside:

- Arguing that economic conditions are not as tight as they look is the “plucking theory” of the business cycle, first proposed by Milton Friedman. It argues that, rather than the current view of the output gap that imagines it operates above potential roughly as often as it is below potential – instead the economy is occasionally plucked well below its potential by a recession, before rebounding back to its potential (but not generally beyond). If correct, the U.S. economy may actually be nearing its potential rather than exceeding it. We find this theory attractive, as we have never particularly liked the idea that economies can operate above their potential for any period of time – if this were truly possible, the potential must be higher than once imagined.

- Conversely, arguing that economic conditions are tighter than they first appear, it has been observed that output gap estimates tend to be revised upwards after the fact. That is to say, an economy that appears to be operating below its potential is later found to have been operating at potential, and an economy that appeared to be functioning at its potential is discovered to have been overheating. This is most obvious late in the cycle. As a result, there is a good chance that when statisticians eventually revisit the current average output gap estimate of +0.8ppt, they will conclude that it was already in line with prior historical peaks.

- Can we reconcile these two seemingly competing interpretations? Yes. On a level basis, we are primarily persuaded by the first argument – that economic conditions are not quite as tight on an absolute basis as they first appear. Perhaps the U.S. economy isn’t actually operating beyond its potential. But keep in mind that this applies to past cycles, as well. None of them were likely as overheated as the conventional estimate shows. And yet apparently simply reaching the economy’s full potential made them slippery enough to slide into recession. The recession risk doesn’t change. Meanwhile, the main thrust of the second claim is that – setting aside levels – the economy is probably tighter than it currently looks relative to past cycle peaks (whatever the absolute level of the output gap). Thus, the business cycle may be farther along than otherwise imagined.

- We can increase the robustness of the output gap estimates by coming up with some alternate measures of economic slack ourselves:

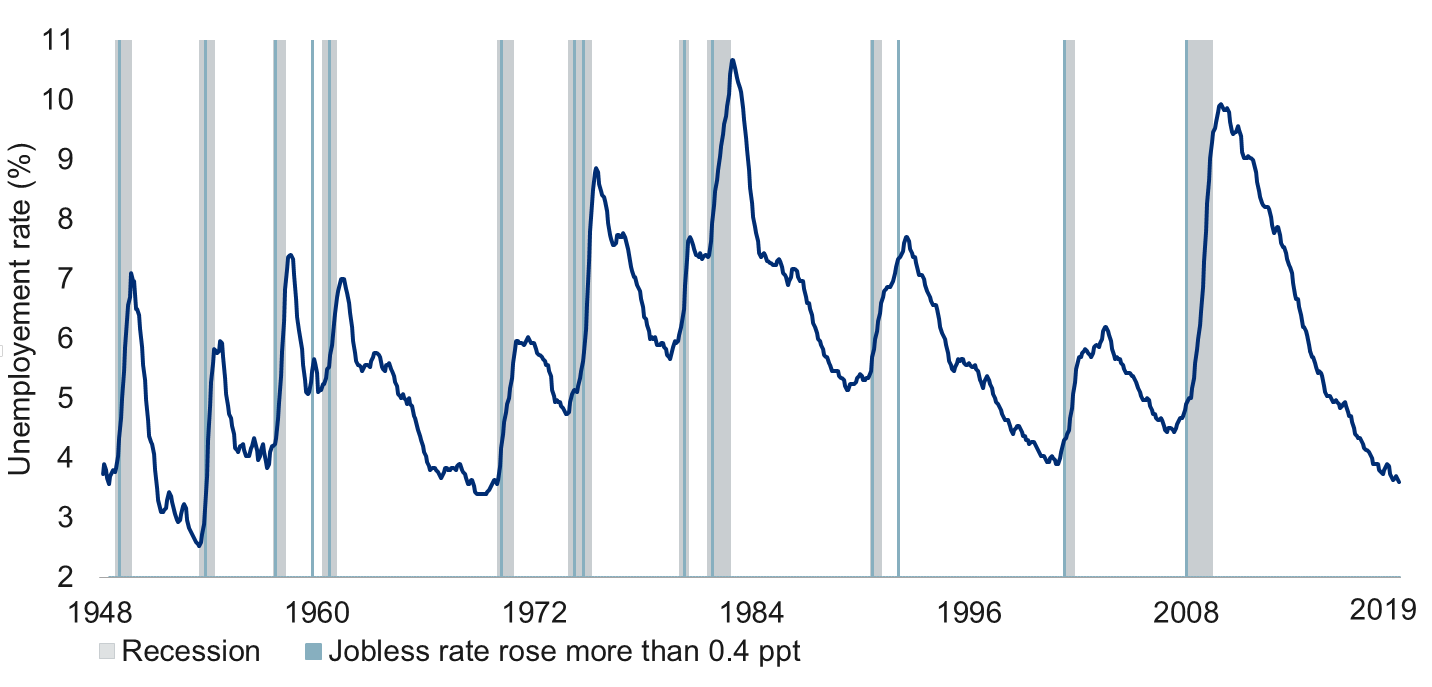

- A superficial examination of the U.S. unemployment rate shows that it is now very low – lower than at any point over the past five decades (see next chart). Using a modern estimate of Okun’s Law (a coefficient of 1.0) and assuming a natural rate of unemployment of 4.5%, this argues the U.S. economy is operating +0.9ppt past its potential, even more than the average of the other measures.

-

Important not to overheat U.S. labour market

Note: As of Oct 2019. Unemployment rate is 3-month moving average. Source: Bureau of Labor Statistics, NBER, Haver Analytics, RBC GAM

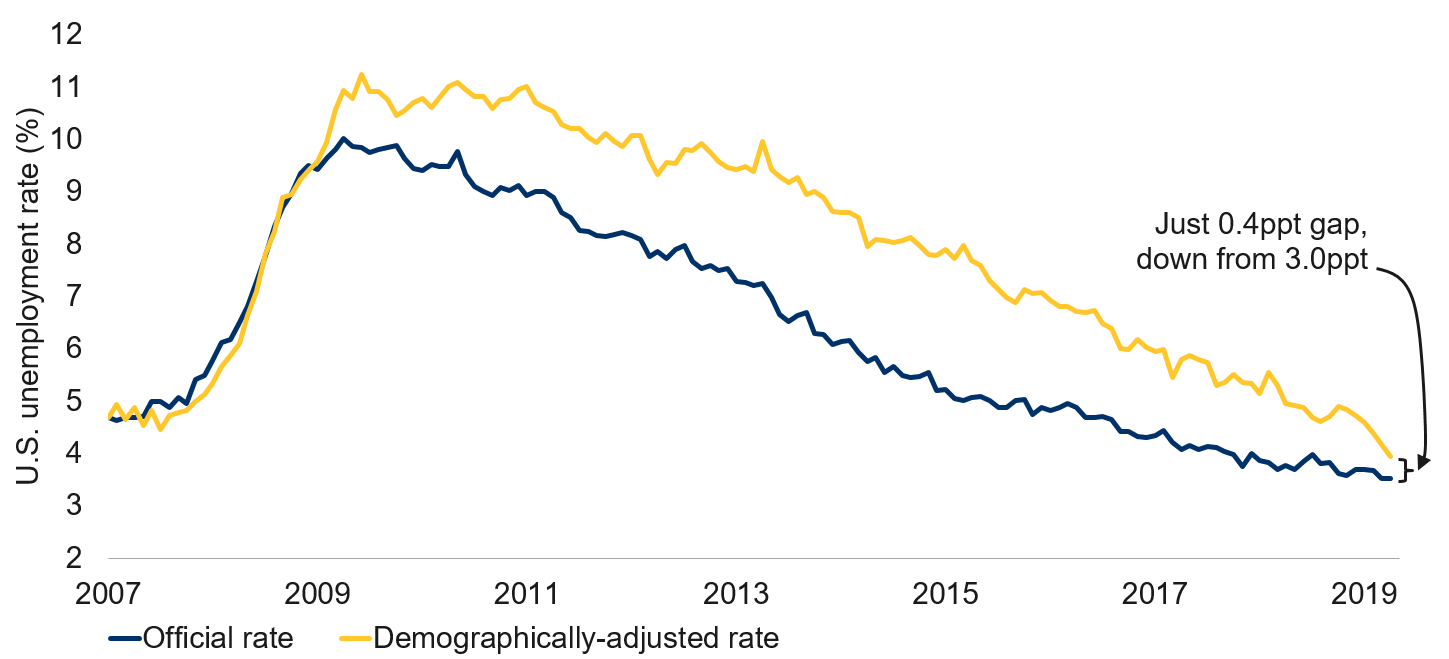

- However, this approach is frequently criticized because it ignores the fact that the unemployment rate excludes discouraged job seekers. There were many such people after the global financial crisis, as evidenced by a significant drop in the labour force participation rate, from a peak of 66.2% to just 62.3%. Fortunately, this has since partially rebounded to 63.3%. Moreover, much of the original decline can be chalked up to an aging population (with more retirees) rather than discouraged job-seekers. Indeed, our demographics-adjusted labour force participation rate has now rebounded all the way to 65.8%, marking a nearly complete recovery.

- In turn, our demographics-adjusted unemployment rate now sits at 3.9%. This is very nearly as strong as the official 3.6% reading, and a massive winnowing of the gap from the huge 3 percentage point differential that once prevailed (see next chart).

-

U.S. unemployment rate is almost as good as it looks

Note: As of Oct 2019. Demographically adjusted rate accounts for ageing population via lower unemployment rate and participation rate. Source: Haver Analytics, RBC GAM

- When this demographics-adjusted unemployment rate is converted into an output gap equivalent, it lands at +0.6ppt. This is still a position of moderate excess demand (refer back to the earlier bar chart).

- To be sure, there are plenty of other complications that render the use of the unemployment rate imprecise, such as a 2017 Fed study that finds 17% of people not in the labour force nevertheless participate in the gig economy, a rising proportion of 20-somethings who are out of the workforce pursuing post-secondary education, a rise in the number of part-time workers, increasing retirement ages, and so on.

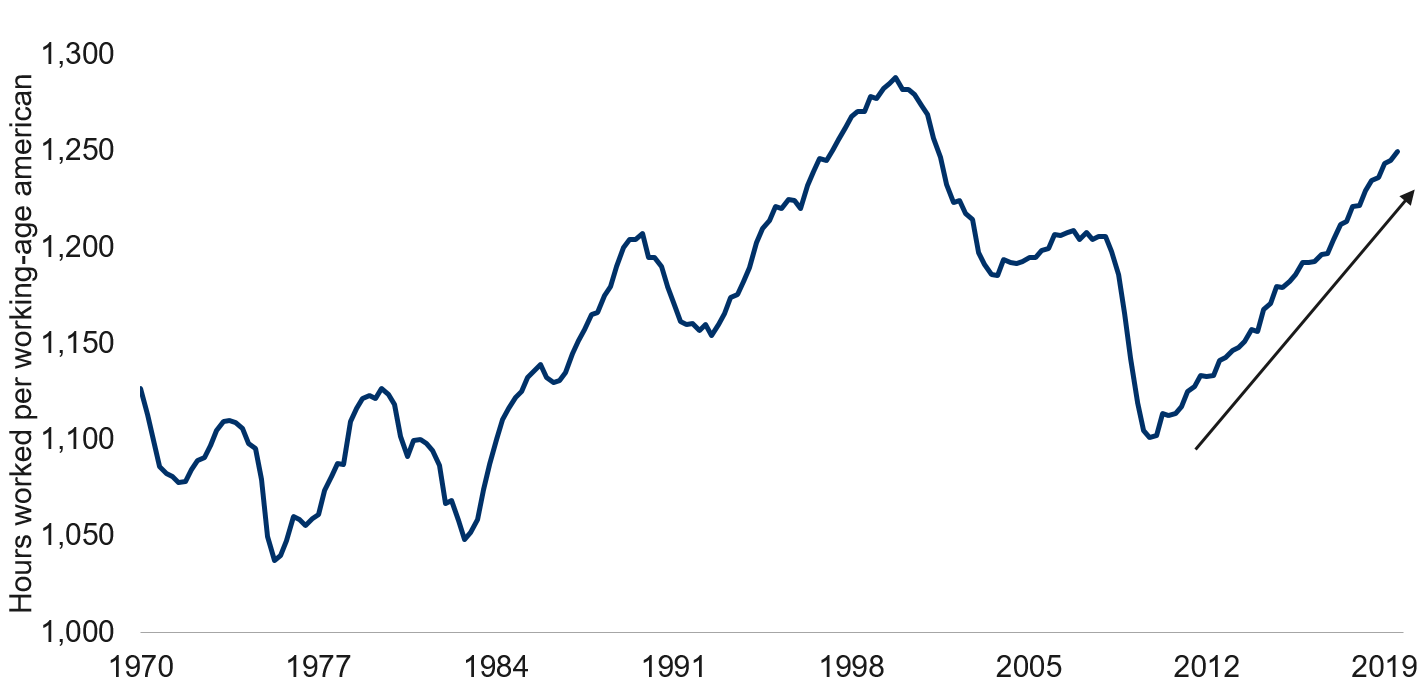

- One way to try and cut through the complications is to set aside the unemployment rate and simply focus on the numbers of hours worked in the economy relative to the number of working-age individuals (see next chart).

-

Hours worked per American are increasingly high

Note: As of Q3 2019. Source: Macrobond, RBC GAM

- There are competing arguments regarding whether these output gap measures are biased to the upside versus the downside:

- This measure argues that the U.S. labour market is now tighter than it has been at any time outside of the 2000 cycle. That is probably not a bad estimate, though it is also imperfect in that the measure captures the total number of hours worked, but then divides by the population aged 16-64. To the extent there are many workers aged 65+ (a rising number in absolute terms, and a rising fraction that are working in relative terms), this probably exaggerates the tightness. Similarly, given the structural increase in formal female employment across the latter half of the 1990s, it is perhaps not surprising that the figures of today are higher than in the past. In the end, there is no perfect measure.

- Where does all of this leave us? The main thrust is that there are many measures of economic slack that all argue the U.S. economy is operating fairly close to historical peaks. In turn, while the steepening of the yield curve convincingly argues that the near-term recession risk has declined, other more persistent measures such as the output gap indicate that the business cycle has not completely reset itself.

Trade roundup:

- There continues to be more good news than bad news on trade.

- Capturing surprisingly few headlines, 15 of the largest Asian nations have tentatively struck a major new trade deal called the Regional Comprehensive Economic Partnership (RCEP):

- The accord, set to be signed in early 2020, encompasses a remarkable 30% of the global economy. The participating countries include such behemoths as Japan, China, South Korea and Australia.

- India has been expected to participate, but has pulled out at the last minute.

- We have two further thoughts to share on the subject.

- First, while globalization no longer glides forward, it is not actually in widespread retreat. Recent major deals include the RCEP, the earlier CPTPP deal, and various new partnerships between the EU and each of Canada, Mexico and Japan.

- Second, the recalibration of global power continue. While the U.S. is retreating from global trade, other nations are forging ahead.

- Turning to the USMCA deal between the U.S., Mexico and Canada, U.S. ratification appears increasingly plausible after comments from U.S. House Democrat leader Pelosi that suggests U.S. politicians are on the cusp of reaching an agreement over enforcement mechanisms to ensure Mexico abides by labour and environmental laws. This would then require re-approval in Mexico and final ratification in Canada, but this seems likely on both counts.

- U.S. auto tariffs have been delayed for the moment, and one hopes permanently to the extent that the U.S. is already pursuing more comprehensive trade deals with practically every country of significance that sells cars into the U.S. (Japan, South Korea, Mexico, Canada, EU).

- U.S. European negotiations remain fairly quiet.

- Finally, U.S. China trade relations have certainly improved over the past few months as talk of a Phase One deal has heated up. At a minimum, scheduled tariff increases have been delayed, which is a victory in itself. We suspect the December 15 tariff increase will also be deferred. There is a real chance of a “skinny” trade deal that would result in China buying more U.S. agricultural products. This becomes even more plausible as the U.S. seeks to restore economic growth with the 2020 election approaching. But we remain dubious there will be a bigger, deeper agreement given ongoing disagreements over enforcement mechanisms, intellectual property practices and state-owned enterprises.

We now turn to a variety of interesting tidbits…

Weak Chinese data:

- China recorded a weak round of economic data releases for October. Retail sales and industrial production underperformed expectations, landing at just 7.2% year over year (YoY) and 4.2% YoY, respectively. These are low by Chinese standards, particularly given they are nominal rather than inflation-adjusted estimates.

- As for whether there continues to be evidence of prior Chinese stimulus trickling through, the story is blurrier than before. M2 money supply growth continues to rise at a solid 8.4%, but credit growth slowed. In fairness, there was a significant seasonal component to the deceleration and the credit trend remains slightly upward. But the story has become a bit less compelling.

- At a minimum, we flag the potential for China to deliver more economic stimulus as an important upside risk to our forecasts.

Japan promises fiscal stimulus:

- After some speculation last summer and a growth-dampening tax hike on October 1, Japanese Prime Minister Abe has now confirmed there will be additional fiscal stimulus delivered in the near term.

- Details are still scant.

- We flag this as yet another example of countries beginning to pivot toward more fiscal stimulus. Recall earlier initiatives from China, India, Germany and the Netherlands. More is likely.

U.S. Democratic race:

- The tentative entry of former New York City mayor Michael Bloomberg into the Democratic presidential race has excited financial markets as Bloomberg represents something of an ideal candidate from a financial market perspective: a pragmatic centrist with a strong business background.

- He has not yet formally declared his candidacy, though the paperwork he recently filed in Alabama is the most serious step he has ever taken in that direction.

- Betting markets give him no more than a 7% chance of capturing the Democratic nomination. This is partially due to his late arrival, partially because Democrats seem more inclined toward far-left candidates this cycle, and partially because he may split the moderate vote with Joe Biden. For this last reason, many argue that Elizabeth Warren is the biggest winner if he does formally enter the race.

- Indeed, Warren continues to lead all candidates with as much as a 26% chance of winning the Democratic nomination, versus 23% for Joe Biden and 21% for a surging Pete Buttigieg. That said, her chance of winning the nomination has earlier crested above 50%, so the race is far from done.

Trump impeachment hearings:

- Democrat-led impeachment hearings of President Trump are now underway, with betting markets assigning a 79% probability that Trump will be impeached by the House of Representatives by the end of his first term. However, the same markets only assign a 6% chance that Trump is not the president at the end of 2019, signaling that the odds of the Senate opting to convict are low.

- We assign an even higher probability of impeachment and a lower probability of his ouster.

Sweden unwinds negative rates:

- Despite ongoing economic weakness and widespread easing elsewhere in the world, it is highly notable that Sweden is opting to reverse its policy of negative interest rates.

- This represents a philosophical change of view – Sweden now believes that negative interest rates may do more harm than good.

- We are fully aligned with that view – the distortions that arise from negative rates are such that it is probably best for central banks not to venture below 0%.

- Does this predict that other central banks such as the Bank of Japan and the European Central Bank may also reject their negative rates? Probably not in the near term, though it probably means they won’t be going any more negative. We do feel it further reduces the (slim) odds that the U.S., U.K. or Canada would opt to venture below 0% even in a scenario of great economic weakness.