More on U.S.-China trade:

- Of the three macro problems that furrowed the market’s brow late last year, two have since been substantially remedied: interest rates are no longer rising and economic growth has slowed its descent.

- The third problem – protectionism – remains unresolved. Elements have admittedly improved since the end of 2018: auto tariffs have been delayed for six months, steel and aluminum tariffs were recently waived for Canada and Mexico, and Congress is becoming less frigid toward signing the USMCA trade deal.

- However, the most important component of the trade landscape – the U.S.-China relationship – has significantly deteriorated.

- Reports of negotiating progress had seemed so promising through the winter and spring. This culminated in what was said to be a 150-page report filled with Chinese pledges to refashion its system of state-owned enterprises, intellectual property practices, joint-venture requirements and capital controls in a way that would put the country on a more level playing field with its peers.

- However, when negotiators put the document in front of Chinese President Xi, he reportedly chopped 45 pages, including the great bulk of the commitments to enshrine changes into Chinese law. Without these, the proposed trade accord was not only substantially reduced but largely toothless.

- China’s reluctance to sign onto a new deal is understandable in that the document was primarily one of Chinese concessions, with few American ones. Why would China sign onto something like this?

- Of course, the opposite perspective is that China’s current trade model affords it significant advantages over the rest of the world. The rest of the world is simply asking that China operate in a more symmetrical fashion. That requires changes from China.

- Ultimately, these different perspectives will be resolved by the question of how long China and the U.S. are willing to tolerate the economic pain of tariffs. The U.S. responded to China’s altered proposal by substantially increasing the tariff rate on Chinese imports (and China has reciprocated).

- There is still a glimmer of hope in that Presidents Trump and Xi will meet at the G20 meeting in late June.

- However, our base-case forecast is now that the latest volley of tariffs will stick.

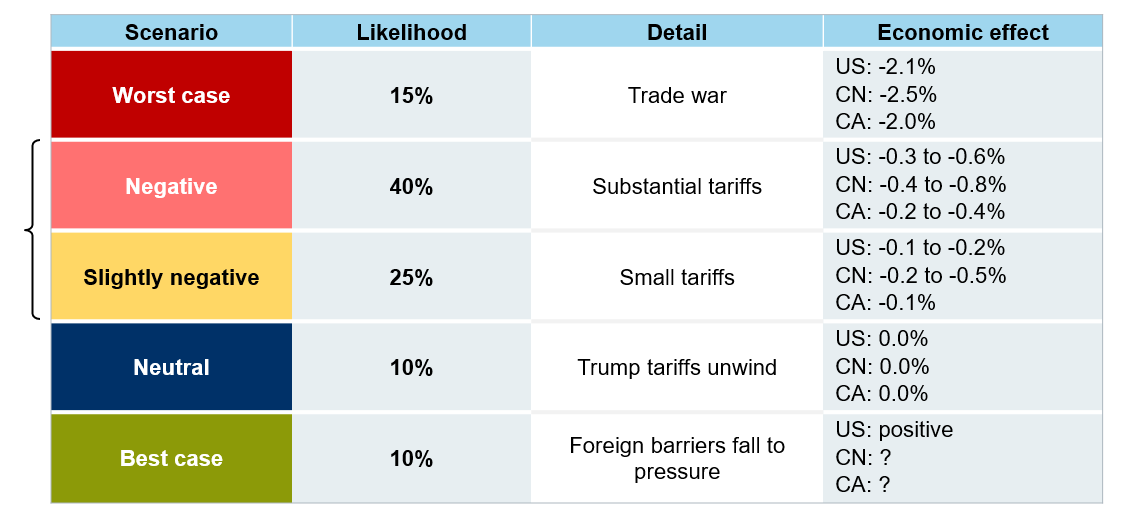

- This conclusion has prompted us to refresh the various models used to calculate the economic damage from protectionism (see chart). The models generally yield damage estimates that are toward the low end of the back-of-the-envelope calculations we submitted in recent weeks. For instance, the U.S. loses between 0.3% and 0.6% of output should current tariffs persist (we previously estimated -0.6%). The Chinese GDP hit will fall between 0.4% and 0.8%.

-

Trade scenarios tilt toward “Negative”

Source: RBC GAM, Oxford, Bloomberg, OECD, Nomura, Goldman Sachs, UBS, Barclays, Fajgelbaum et al

- If these figures seem small, it is worth noting several things:

- First, it is the very nature of businesses to profit maximize. They will only continue to import a product subjected to a pricey tariff if they cannot find a cheaper substitute at home, find an alternate foreign supplier, or find a way to function without the product altogether. Not infrequently, one of those options proves feasible.

- Second, if U.S. businesses can prove that no alternative domestic supplier exists, they can apply for a tariff waiver – 80,000 such requests have been submitted regarding steel and aluminum tariffs alone. Processing them expeditiously has proven to be a problem, however.

- Third, governments frequently assist affected industries. The U.S. has directed billions of dollars to help its agricultural sector survive Chinese tariffs, as an example. This replaces economic damage with a higher public debt.

- That said, we have reason to think that the models may fail to capture the full extent of the damage:

- First, even the models acknowledge that the welfare loss to households and businesses is larger than the cumulative economic damage. This is because the government sector frequently comes out ahead thanks to the extra tax revenue it is able to collect via tariffs. Other sectors are thus left even further behind.

- Second, some domestic parties benefit when foreign competitors are blocked from the market. But that means that consumers and companies reliant on foreign inputs are hurt even more than the aggregate economic numbers suggest.

- Third, and most importantly, the models completely miss the fact that governments are also engaging in protectionism via non-tariff means (see next chart). This damage goes unquantified, but is ultimately very real.

- Fourth, the stock market tends to respond by a multiple of several times that of the economy to shocks such as these. As such, a multi-percentage point move in the stock market is perfectly reasonable for a protectionist shock that only knocks half a percentage point off economic growth.

-

Trade war ammunition extends well beyond tariffs

Source: RBC GAM

- Of the non-tariff barriers, corporate attacks have been the most obvious means of cross-border antagonism. The U.S. first hit Chinese telecom giant ZTE last year, before famously targeting tech champion Huawei this year. For its part, China has blocked a Qualcomm merger proposal, levelled anti-trust allegations against chipmakers including Micron, and has limited the sale of certain Apple products within China.

- Huawei, in particular, finds itself at the centre of attention. Not only has its CFO been charged by U.S. courts and its 5G products blocked in the U.S. and several other developed nations. Now, American companies must obtain government permission to engage in commerce with the company – effectively blocking further business. This means Huawei can no longer rely on many key American technologies used in the company’s products. Other issues include:

- On the software side, the rules crimp Huawei’s ability to continue using the Android operating system in its phones. Among other things, Huawei is the world’s second largest mobile phone producer.

- Non-U.S. technology suppliers are now treading cautiously around Huawei.

- The company has been blocked from future participation in two tech standard organizations that negotiate universal protocols for such technologies as Wi-Fi and SD memory cards.

- So far, Huawei has not been blacklisted on the dollar clearance system – a step that nearly bankrupted ZTE in 2018 before the U.S. hastily reversed its edict.

- Huawei has likely been targeted for a mix of reasons:

- The country is leading the 5G charge, with no U.S. competitor in sight. As such, part of the U.S. effort may be simply to limit the extent of China’s technological lead.

- Huawei is alleged to have acquired a significant fraction of its foundational intellectual property in questionable ways, often at the expense of leading developed-world firms.

- The U.S. accuses Huawei of violating U.S. sanctions on Iran, though the company professes its innocence.

- The U.S. worries that Huawei’s close proximity to the Chinese state could result in espionage should countries place the company’s 5G products at the heart of their telecommunications networks.

- Huawei’s restrictions could well be resolved by any trade pact between the two countries. Setting a precedent, ZTE’s limitations were eventually lightened as a favour to the Chinese president – an entirely political decision rather than a legal one.

- U.S. actions risk backfiring if implemented for too long. The longer China loses access to U.S. technologies, the more likely it is to replicate such technologies itself. Similarly, any loss of access to the U.S. dollar clearance system would serve to accelerate the creation of a competing Chinese clearance system, undermining America’s ability to exert the same clout in the future.

- China also possesses the ability to hit the U.S. via non-tariff means, be it selling U.S. Treasuries, restricting the sale of Chinese-made iPhones or similar prestige products, or even halting the export of rare Earths (it has a near monopoly) that find their way into all modern electronics.

- The bottom line is that serious economic damage is being done via newly elevated tariffs and aggressive non-tariff actions. For the moment, we assume that existing measures stick, but do not budget for any significant alleviation (or intensification) in the near term.

British politics:

- British Prime Minister Theresa May has announced her resignation, effective June 7, 2019.

- This is far from a shock. She has been under pressure from her cabinet for some time, and had previously promised that she would resign in the coming months. However, the announcement brought forward this date slightly.

- Recall that her Brexit plan negotiated with the EU had already been formally rejected three times by parliament. The first of these was voted down by a record margin. Efforts to negotiate across party lines had not borne obvious fruit, and May was seemingly on track for a fourth rejection in early June even after having made a few amendments to the plan.

- The next Conservative Party leader and thus Prime Minister will be selected by late July. The process is an interesting one: several rounds of voting by MPs will occur, with the least popular candidate removed each time. When the list has been whittled down to just two names, these candidates are then put to the country’s Conservative Party membership, which votes on the winner.

- The latest polling shows former London mayor and ex-cabinet minister Boris Johnson well in front, with three times the support of the next most popular candidate. Johnson supports Brexit, but is fairly centrist within the party, having voted at one point for Theresa May’s proposed deal with the EU.

- The second most popular candidate is Dominic Raab. He is further to the right and claims to prefer a chaotic “no deal” Brexit to the options currently on offer from the EU.

- While it might seem that Johnson should be a slam dunk to be the next Prime Minister given his clear lead, betting markets only assign him even odds versus the field. Do not forget that the Conservative Party membership is further to the right than the average Conservative voter, and the average Conservative voter is further to the right than the average British citizen. Furthermore, while Johnson would stand a large advantage in a pool of many candidates, the final voting will contain just two options. The hard Brexit supporters may be able to congeal around a single candidate currently subsumed in a sea of ideologically similar candidates.

- It is undeniable that Theresa May’s exit as Prime Minister increases the risk of a harder Brexit. While a Prime Minister could not secure a hard Brexit agreement with the EU all by themselves, they could theoretically force a “no deal” Brexit. This would be a bad economic outcome. However, there are more positive outcomes, too. Parliament still has a say in most scenarios, and its composition of members remains tilted toward a softer version of Brexit. Conceivably, Boris Johnson as prime minister could have more luck pushing a Theresa May-type deal across the finish line with the benefit of a fresh mandate.

- It often goes forgotten that the bulk of Brexit negotiations continue to focus on the nature of the transition arrangement rather than what the U.K.-EU relationship will ultimately look like. The latter is ultimately far more important, and we continue to give our nod to a customs-union type relationship given the way in which it could sidestep problems surrounding the free flow of people and the thickness of the Irish border.

- For now, the October 31, 2019 deadline still applies for finalizing the transition arrangement. Germany is sympathetic to a further extension if needed, while France is less so. Betting markets assign a 50% chance that Brexit is not resolved before 2022. The saga continues…

European politics:

- The EU election results were made public over the weekend, yielding a populist outcome, though not exactly the one that was expected. While centrist parties suffered losses and far-right parties enjoyed significant gains, the far left unexpectedly achieved even more growth.

- The far-right had commanded 20% of the seats before the election, managing to increase its support to 25%, but not to the 33% that had been expected.

- Populism is clearly thriving, but has not yet wrested control away from the centrists.

- It appears that a coalition of centrist parties should retain control in the European parliament, though they may require support from a more left-wing party to govern effectively. This suggests less legislation overall, and perhaps a tilt toward more environmentally-friendly policies.

- For its part, the U.K. fraction of the vote went as expected. The Brexit Party captured 32% support, nearly double that of the next most popular party (Liberal Democrats). Labour languished in third place, while the Conservatives were crushed with just 9% support in fifth place. What explains the particularly anti-establishment tilt of the British contribution?

- It is not that most Brits now support Brexit. Polls have consistently shown that slightly more British citizens prefer to remain than to leave.

- Instead, it is likely a function of several things. Turnout is always low, meaning only the most motivated voters bother to participate. This election’s importance was even lower than usual from a British perspective, because whoever is elected is unlikely to be in Brussels for long if Brexit succeeds. Only people with an axe to grind bothered to vote, and so it is no surprise that this skewed toward Brexit supporters frustrated by two years of inaction. Even those with more mixed views on Brexit can hardly resist punishing the EU for playing hardball in negotiations so far. This also explains why the Conservative party – which has been in charge of the British side of unsuccessful negotiations – also fared so poorly.

Indian election:

- The world’s largest democracy just concluded its seven-step election odyssey, resulting in 600 million votes cast – the largest election in history. Incidentally, the second largest recurring democratic event in the world is the aforementioned EU elections.

- The big news in India is that Prime Minister Modi and his BJP party not only won, but captured an even larger majority in the lower house than the prior election. For much of the run-up to the election, the expectation had been for a diminished margin.

- This was a market positive event, not merely because of the continuity it offers, but because the Indian economy has performed fairly well under Modi. GDP growth has trended at around 7% per year, even if labour market metrics have been less impressive.

- A lingering item to watch is the nationalist streak Modi has occasionally demonstrated, first as the Chief Minister of Gujarat and more recently as Prime Minister.

Canadian GDP preview:

- Canadian Q1 GDP will be released later this week. It stands a good chance of beating the Bank of Canada’s meagre forecast. It could potentially land in the realm of +1.0% annualized, significantly aided by the prospect of a happy +0.3% (unannualized) gain in the final month of the quarter.

- However, let us be clear that 1.0% growth does not constitute a good quarter in any absolute sense. It runs at around half the trend rate, and promises to be a second consecutive quarter of underperformance.

- The curious thing about the Canadian economy is that the labour market numbers, to the contrary, have been extraordinarily strong.

- There really is no reconciling the two – it simply doesn’t make sense, and is unlikely to last for long. While they may meet somewhere in the middle, we are inclined to think that hiring will be forced to slow more substantially than GDP will accelerate.

Bank of Canada preview:

- The Bank of Canada’s overnight rate is likely to remain unchanged at its meeting later this week.

- There have been a few negative developments of late, including deteriorating U.S.-China relations and slightly lower oil prices.

- However, recent positive developments arguably outweigh the bad. These include:

- The Canadian dollar is a little softer than last time.

- The global economy has grown a few green shoots.

- Q1 GDP is likely to clear the low bar set for it by the central bank.

- Job growth has been vigorous.

- This adds up to a slightly better situation overall, as demonstrated by market expectations that now price in a smidgen of a chance of a rate hike (though it is still quite unlikely) versus no chance of a rate cut.

- However, the tables turn further out with a quarter of a rate cut priced by September, versus just 8% of a rate hike.