Recession risk

- Amid slowing global growth, trade protectionism and late-business-cycle readings, the risk of recession has indisputably risen over the past year.

- There are many ways to estimate of the recession risk, ranging from sophisticated econometric models that attempt to quantify the various impulses rippling through the economy, to counting the frequency with which the word “recession” appears in online newspaper articles, to the slope of the yield curve.

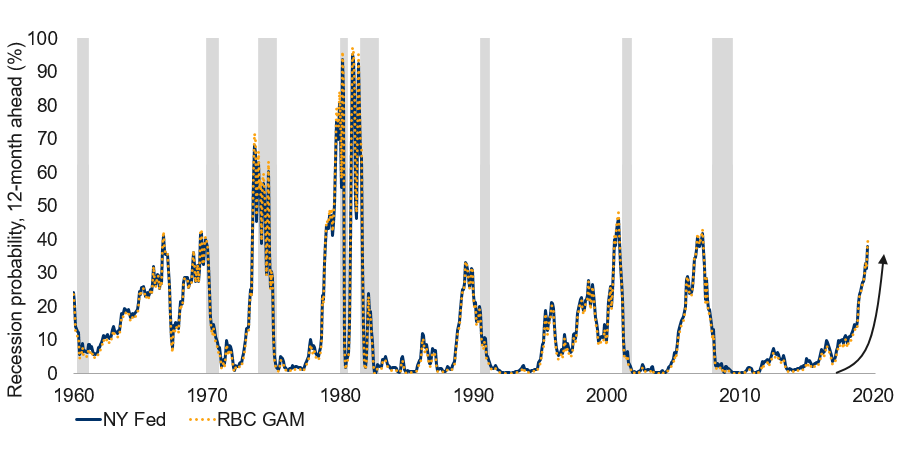

- With regard to the last of these – metrics that attempt to translate the yield-curve slope into the probability of recession—the New York Federal Reserve Bank (New York Fed) publishes the most prominent one for the U.S. economy. Alas, the metric is only published once a month. This would normally suffice, but in recent months the bond market has gyrated with such force that the model’s predictions have rapidly grown stale. The measure was obviously outdated through August, when yields had fallen and the yield-curve had further inverted since the prior estimate.

- To remedy this, our team has replicated the New York Fed’s indicator in an attempt to gain a real-time gauge of the recession risk identified by the bond market.

- The New York Fed’s measure suggested that the risk of recession over the subsequent 12 months was a sizeable 31% as of late July, and this was recently updated to a 38% chance as of late August. Our own higher-frequency version of this now flags a 44% one-year recession risk as of early September (see the chart below for both versions).

-

Yield-curve-based U.S. Recession probability surges

Note: As of Aug. 2019 for New York Fed model, RBCGAM estimates as of 9/3/2019. probabilities of a recession twelve months ahead estimated using the difference between10-year and 3-month Treasury yields. Shaded areas represent recession. Source: U.S. Federal Reserve.

Some additional context is useful:

- Optimists should note that the bond market is likely still distorted by the vestiges of quantitative easing, with the yield curve probably flatter than it would otherwise be as a side-effect. In turn, one can argue that the recession risk may not actually be as high as the model is claiming. We also believe that the next recession may be a fairly mild one from a depth perspective.

- However, pessimists should be aware that, going back more than fifty years, a recession has always happened once this metric has risen above 30% (though sometimes not for a year or two). Furthermore, the current reading is already higher than the model ever got before the financial crisis, and is nearly as high as before the prior recession. Such models work differently than commonly imagined – they rarely peak out anywhere close to 100% even when a recession does happen. Of course, given the infrequency of recessions, we are stuck working with a remarkably small sample size of data, so nothing is certain.

- A 44% chance of recession is several times higher than normal. We interpret it to mean that a recession should not be one’s base-case expectation for the next year, but it comes a close second place. That is consistent with the way we have managed our own tactical asset allocation – with less risk on the table that at any point in several years, but maintaining a decent exposure to risk assets like equities given that there is still a fair chance that recession is avoided, and given superior long-term prospects for such investments.

- For what it is worth, former Harvard President and public intellectual Larry Summers recently opined that he puts the U.S. recession risk “just below 50%” by the end of next year.

- Were the recession risk to rise further, such as to 55%, it is important to recognize that while this would technically make a recession more likely than not, continued economic growth would still be nearly as likely. Additional caution would be appropriate for investors, but this should not be viewed in a binary fashion: incremental shifts in risk require incremental shifts in investing behavior.

- A final side note as we continue to watch this indicator. It is interesting that, historically, the assessed recession risk has fallen from its high before the recession actually began. Why? From a mechanical perspective, the yield curve usually starts to re-steepen when a recession is truly imminent. This happens because central banks pivot to aggressive easing, pulling the short end of the curve downward. From a theoretical perspective, the model is also correct in ascribing a diminishing recession risk – the model’s job is to predict a recession in one year’s time, not tomorrow. When a recession is just a few months away, there is a high probability that the economy will be back to growth twelve months later. This creates an obvious headache, in that we cannot automatically breathe a sigh of relief should the reported recession risk start falling. Fortunately, there is a way to determine whether the declining probability is good or bad news. If the model’s output is falling while long-term yields are themselves declining, it is probably because a recession is getting near. If the model is falling while the long-term yield is rising, it is probably because the recession risk is actually fading. - With contribution from Vivien Lee

Canadian provincial update:

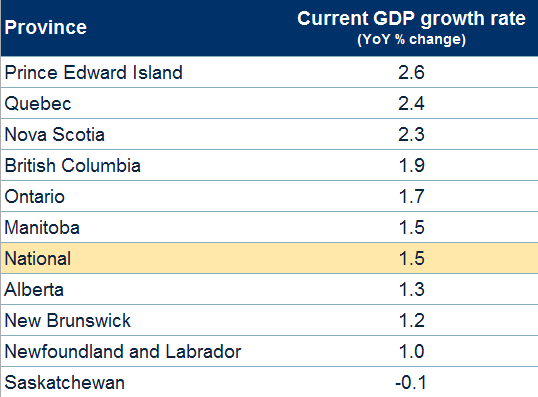

- We have updated our proprietary Canadian provincial GDP models, yielding the following results (see chart).

-

Note: National GDP as of Jun 2019, RBC GAM estimates of provincial GDP year-over-year growth rate as of Jul 2019. Source: Macrobond, RBC GAM

- Relative to national GDP growth of 1.5% YoY through the middle of 2019, our model estimates that Prince Edward Island, Quebec and Nova Scotia significantly outpaced that average with growth ranging from 2.6% to 2.3% YoY.

- British Columbia and Ontario land just above the national average with pedestrian growth of 1.9% and 1.7% growth, respectively.

- Manitoba, Alberta, New Brunswick and Newfoundland and Labrador report growth at or moderately below the national average, in a range of 1.5% to 1.0%. Of course, while Alberta and Newfoundland are managing limited growth, they are still suffering from the earlier oil shock that has left their unemployment rates higher than normal.

- Lastly, Saskatchewan appears to be trailing the other provinces significantly, with an economic decline of 0.1% over the past twelve months. We hypothesize that this is at least partially the result of a challenged energy sector paired with the effect of China blocking various Canadian agricultural products.

Hurricane Dorian:

- We wrote about how hurricanes can affect economies last week. Hurricane Dorian has now dealt most of its damage, allowing for an initial assessment of the economic costs. By far the worst hit was to the Bahamas, which suffered tragic loss of life and severe destruction estimated at US$7 billion.

- The U.S. was not entirely spared, with coastal North Carolina in particular suffering damage, but the hurricane took a fortuitous route that kept it largely offshore as it ventured up the U.S. coast. Accordingly, the material damage and economic consequences appear to be far less than infamous hurricanes of years past such as Katrina, Sandy and Harvey.

- Canada suffered a not-inconsiderable blow, with Nova Scotia and parts of New Brunswick subjected to the post-tropical storm effects of Hurricane Dorian. Whereas Hurricane Juan (2003) inflicted an intense blow to a small part of the province, Dorian’s effect was more broadly felt. Reports indicate power outages for as many as 400K households – a startling number given that the entire province has just 459K private dwellings. The affected number is already declining nicely, reported at below 300K less than 24 hours later, but there will clearly be some lost economic output and damage to contend with. That said, downed tree limbs appear to be the primary damage, as opposed to destroyed homes. As such, the economic consequences will probably be fairly limited. For context, Hurricane Juan inflicted roughly $300M of damage 16 years ago. This sort of effect is likely large enough to show up in Nova Scotia’s provincial GDP (discussed earlier), though the province is lucky that it had such good economic momentum going into the episode. The effect may be too small to seereflected in Canada’s national GDP.

Monetary stimulus:

- Central banks continue their attempts to stabilize growth.

- Among them, the ECB is likely to be rendering its verdict on Thursday September 12:

- Mario Draghi’s last meeting will probably be fitting, delivering the fireworks and remarkable dovishness for which he has become known.

- In response to global growth woes, elevated uncertainty and dimming inflation (and perhaps most ominously, low inflation expectations), the ECB seems likely to deliver a multi-pronged stimulus package.

- A deposit rate cut of 10bps to 20bps from the current -0.4% is expected, although its effect should be tempered by a new tiering system that will try to limit the extent to which banks must pay a negative interest rate on their excessive deposits held at the ECB.

- There has been talk that the ECB could also provide a form of conditional guidance – a commitment to foreswear rate increases until such a time as inflation expectations have revived back to normal levels. This seems like it could be a good idea, not so much because it alleviates concern about near-term hiking—there is little worry about that—but more so in that it makes a serious effort to address the Japanification of Europe via withering inflation. The ECB is no stranger to forward guidance – it currently promises no rate hikes through to the middle of 2020, but this would add the twist of a specific economic target as opposed to being bound by an arbitrary calendar date.

- There are expectations that the ECB will step up its quantitative easing – printing money to buy bonds – though it has only limited scope to do so before bumping into its own self-imposed limit regarding the fraction of each bond issue that it is permitted to own (33%). This can likely be circumvented fairly easily.

- The ECB is also rumoured to be planning to deliver additional liquidity to the continent’s banks.

- While we believe much of this anticipated stimulus will be delivered, the risk is that the market may be expecting too much. There are skeptics on the governing council who argue that the unemployment rate is too low to motivate such extreme action. Nevertheless, setting aside the vagaries of markets, the ECB is clearly pivoting toward support, and that is surely a positive thing for economic growth over the coming year.

- Looking forward, Christine Lagarde – previously of the IMF – will replace Draghi in October, and appears likely to prove his equal in terms of her pragmatism and willingness to support growth and inflation.

- The Bank of Canada delivered its own rate decision last week:

- The overnight rate was left unchanged at 1.75%, as expected. Furthermore, the Bank of Canada did not explicitly signal any plan to alter its stance in the near term, indicating that the “current degree of monetary policy stimulus remains appropriate.”

- Of course, the Bank of Canada under its current management has little interest in providing forward guidance to markets. Think back to the surprise rate cut of 2015. As such, the Bank could still easily find its way to delivering stimulus either in late October or at a later date.

- The latest communiqué struck us as notably more dovish than the prior iteration, with plenty of references to weakness, including the escalation of the U.S.-China trade conflict, contracting world trade, weakening global business investment, high uncertainty, a diminished global growth outlook, weaker U.S. growth, lower commodity prices and a forecast that Canadian growth will slow over the second half of 2019.

- There are two sides to every story, but the hawkish elements were notably scarcer, limited to the recent strength in Canada’s Q2 GDP growth, rising wages and stronger than expected inflation (though this was acknowledged as being largely for temporary reasons). Since then, Canada’s August job report arrived with remarkable strength.

- The Canadian case to cut rates is less compelling than in many other markets. Recent domestic indicators, from Q2 GDP to inflation to employment have all been good. However, the U.S. economy has a heavy influence over Canada and the various global risks clouding the outlook are no less relevant for Canada. We still believe there is a high chance that the Bank of Canada finds itself cutting rates within the next year, with a decent prospect that the next meeting in late October could kick things off. Much depends on how the world and Canada proceed between now and then.

- The People’s Bank of China has, for its part, pre-announced a 50bps rate cut scheduled for September 16, continuing a long pattern of monetary easing from the world’s second largest economy. India has also been cutting rates.

- Finally, the U.S. Federal Reserve Board is still emitting signals very much consistent with further rate cuts. We assume 25bps at the next opportunity. A 50bps rate cut would require some further deterioration of conditions or outlook.

Fiscal stimulus:

- So far, monetary stimulus has been the primary instrument of stimulus in the battle against slowing growth. But fiscal stimulus could also conceivably play a role. The 2008-2009 period provides many examples of truly remarkable fiscal stimulus delivered in response to an economic crisis.

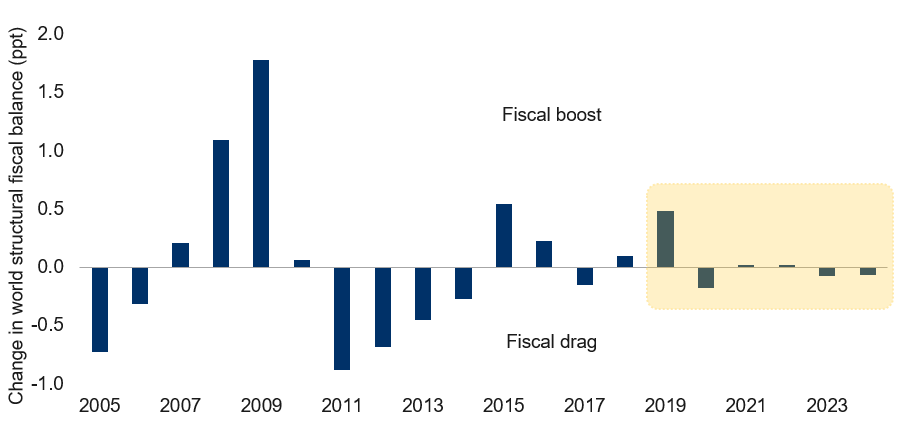

- However, current government budgets fail to highlight any premeditated plan for action. As the IMF has calculated (see next chart), government budgets are actually scheduled to become more restrictive over the coming year, potentially subtracting as much as 0.7ppt from global growth in 2020 relative to 2019, all else being equal.

-

Global fiscal stimulus to be less supportive

Note: Forecast from IMF World Economic Outlook, Apr 2019. PPP-based country GDP as share of world total used as weights. Source: IMF, Haver Analytics, RBC GAM

- But this is not the final word on fiscal stimulus. This is partly because governments tend to exhibit poor discipline – a plan for a surplus can easily drift into a deficit as political desires out-muscle fiscal restraint, even during the best of economic circumstances. For this reason, the IMF probably structurally underestimates the amount of future fiscal stimulus.

- But, in addition to that, slowing economic growth triggers the same alarm bells for fiscal policymakers as it does for monetary policymakers.

- It is no coincidence that China has been delivering substantial fiscal stimulus over the past year at a time when global growth is slowing. Granted, this effort been disproportionately directed at tax cuts that are not proving as powerful as prior rounds of infrastructure spending once did. Nevertheless, there is tentative evidence of this beginning to appear in the country’s credit figures as its credit impulse turns positive for the first time in several years. For the moment, the IMF assumes a return to fiscal restraint for China in 2020, but this could yet change as the country scrambles to meet its 6.0% to 6.5% GDP growth target.

- India is now talking about a sales tax cut on motor vehicles after suffering a stark 41% drop in auto sales over the past year. It should be noted that while some of this slowdown may have an economic-demand underpinning, much relates to the stingier provision of auto loans from the country’s troubled financial sector.

- Germany has publicly stated its willingness to deliver up to 50 billion euros of stimulus and the country undeniably possesses ample fiscal capacity. However, Germany is only willing to unleash this offensive in the event of a deep recession. More generally, Eurozone nations have committed – at least in theory – to keep their deficits to no more than 2-3% of GDP, limiting their role in fending off an economic slowdown. In fairness, this shackle would likely be ignored in the event of full-on economic recession, however.

- The U.K. is likely to deliver more fiscal support in response to high Brexit uncertainty that has damaged growth, but the chaotic state of its parliament makes any precise prediction foolhardy.

- In the United States, the White House recently floated policy balloons relating to a temporary payroll-tax cut akin to that delivered by President Obama during his first term and/or a capital-gains tax cut that would be achieved by indexing returns to inflation. But it is far from clear that anything short of an emergency would induce the kind of cooperation needed to deliver a major fiscal package in the U.S.

- Japan is set to impose fiscal restraint rather than stimulus in the near term as it delivers a long-awaited sales tax hike on October 1. That said, and despite its gargantuan public debt, it is usually up for a round of fiscal stimulus should conditions demand it.

- High public-debt loads are unlikely to constitute a near-term constraint as bondholders are hardly suffering indigestion. What is more, governments can borrow at negative interest rates in Europe and Japan, and for a pittance elsewhere: this makes it entirely possible to deploy fiscal stimulus that effectively pays for itself. Of course, long-term concerns remain as public debt loads are already high by historical standards.

- For all of this enthusiasm, fiscal policy is much better at digging economies out of deep recessions than at preventing them beforehand, for several reasons:

- Lack of coordination: a crisis and/or deep recession have a way of galvanizing political support in a way that a gradual economic deceleration such as the one occurring today just doesn’t.

- Lack of nimbleness: political procedures are cumbersome and fiscal programs usually take months or even years to fully implement.

- Lack of optimization: the pork-barrel politics necessary to deliver a bipartisan fiscal stimulus package is rarely notable for its economic efficiency.

- Lack of economic pop: the fiscal multiplier tends to be smaller when economies are operating near their full potential, as they are today; fiscal stimulus works much better when grappling with a high unemployment rate.

- The bottom line is that countries do appear to be at least awakening to the possibility of fiscal stimulus, although whether they will develop the necessary willpower in time is still an open question. The clear risk is that they do not act until stall-speed has already been undershot and it is too late to recover. China constitutes a potential exception, in the sense that it is globally relevant, less bound by domestic politics, has a history of massive fiscal undertakings, and is already delivering some fiscal stimulus. It merits close watching.

Data run:

- The divide between the manufacturing sector and non-manufacturing sector has again yawned wider. After an ISM Manufacturing print for August of just 49.1 – below the critical 50 threshold and confirming the “manufacturing recession” already visible elsewhere in the world, the ISM Non-Manufacturing index was released last week and managed a healthy rise from an OK reading of 53.7 to a good one of 56.4. The new orders component rose to a strong 60.3. Just for the sake of extra confusion, the Markit Manufacturing PMI rose while the Markit Non-Manufacturing PMI fell. For those keeping score, we continue to believe the manufacturing sector is in the worst position, that the service sector has weakened but is still tentatively growing, and that consumers are the most supportive of the bunch (though with an increasingly visible hit to their confidence, and a decelerating employment trend that we tackle next).

- U.S. payrolls for August arrived at +130K, and this adjusts down to merely +105K after temporary census hires are removed. This is not bad in an absolute sense: it is sufficient hiring to keep pace with population growth, for instance. Nevertheless, it represents the continuation of a slowing trend that has been visible since the middle of last year. The same goes for the unemployment rate (not rising, but no longer falling) and weekly jobless claims (also not rising, but no longer falling). This has the look of an aging labour market.

- Canadian employment recorded a big 81K job gain in August. For a country with barely more than one-tenth the U.S. population, that is something. The details weren’t quite as strong—the unemployment rate remained unchanged at 5.7% and most of the new hires were part-time – but it was undeniably a solid report. Just when we thought we’d started to solve the mystery of strong employment versus weak GDP (prior employment reports had begun to weaken and the latest GDP report strengthened – beginning to bridge the gap), it is widening out again. The mystery persists.

- Brexit update: Brexit prospects continue to swirl. Boris Johnson has lost his working majority in Parliament; Parliament has rejected his pursuit of a snap election and implemented a law that should automatically extend the Brexit deadline by three months if a deal is not struck with the E.U. by the end of October. In this sense, the risk of a no-deal Brexit would appear to be substantially diminished. However, the story is not quite done. There are at least three ways that a no-deal Brexit could still occur: the extension is merely a request that 27 E.U. nations have to unanimously approve – there is a margin for error here, particularly given that the Johnson government will make it known that it does not endorse the parliamentary request for an extension; Prime Minister Johnson has promised to look for loopholes in the law; and there is a convoluted scenario by which Johnson could resign, Labour could take over, and a non-confidence vote could be triggered that forces a snap election and inadvertently a no-deal Brexit. Still, the downside risks are somewhat diminished relative to a week or two ago. Curiously, the odds of a bad Brexit appear to be diminishing at the very moment that the public is more supportive of it than ever (as demonstrated by the polling of the Conservatives under Johnson and the Brexit Party). Much could yet change, and absent a shift in the U.K. or E.U. position, it is still hard to see an actual deal being struck that deviates from what Theresa May put together, leaving a “no Brexit” or a no-deal Brexit.