Monthly webcast:

- Tune in to our latest monthly economic webcast: Central banks vs slowing growth.

Hurricane math:

- Record-setting Hurricane Dorian has already devastated the Bahamas and is now menacing the southeast coast of the U.S.

- The situation is a tragic one, with loss of life already reported plus massive property damage. It is premature to judge the total insurance cost, but estimates are already rising into the tens of billions of dollars.

- Of course, from an economic standpoint, the accounting works slightly differently. The destruction of property and infrastructure is not itself subtracted from GDP. Instead, the GDP impact comes from the interplay of three things:

- Regular economic activity is temporarily halted by natural disasters. People cannot get to work, businesses cannot produce things, and households cannot buy anything. Of this, some is lost forever, while some is recovered once conditions normalize.

- The loss of infrastructure and capital means that economic output in the future may be limited without the full use of ports, bridges, roads and factories for some time.

- Conversely (and perversely) the need to rebuild said ports, bridges, roads and factories (not to mention homes) acts as a stimulant to GDP as construction activity must rev up to levels above where it would otherwise have been.

- The net effect is usually negative, at least in the short run, though a fair chunk of the initial short-run damage is usually unwound over subsequent months and quarters.

- From a U.S. perspective, much will depend on how extensively the hurricane makes landfall, the length of any electrical outages, and of course the physical and human toll.

- For context, Hurricanes Harvey and Irma (2017) and Hurricanes Katrina and Rita (2005) were the two most damaging hurricane seasons in modern U.S. history.

- The White House estimates that annualized Q3 2017 GDP was reduced by around 0.6ppt (-0.15ppt off 2017 annual GDP) as a result of the hurricanes. The Congressional Budget Office figures that Katrina and Rita eventually did as much as 1.0ppt to 1.5ppt of damage (-0.25ppt to -0.3ppt off 2005 annual GDP). From an employment perspective, September 2017 employment was temporarily hit by 140K jobs. In 2005, the damage was 230K jobs.

- Chances are that this hurricane will prove less damaging than those. But the pertinent question today is whether a vulnerable economy already grappling with slowing growth, fragile confidence and late-cycle indicators can handle even a temporary shock such as this. The timing isn’t helpful, in any event.

Manufacturing bad news:

- A mere week after we celebrated the tentative stabilization of a range of global purchasing manager indices (Europe, U.K., Japan, Canada), it is emphatically clear that the U.S. is not partaking in the festivities.

- The U.S. ISM Manufacturing Index for August has just fallen from 51.2 to 49.1, substantially undershooting expectations and landing on the wrong side of the 50 threshold that separates manufacturing-sector growth from decline. Within the index, new orders fell to 47.2. The employment sub-index also dipped below 50, to 47.4.

- To be clear, a manufacturing sector in decline is:

- Not entirely shocking, given that core capital goods orders have already been reported to be down on the year, and given that several other countries’ manufacturing indices had already found their way below 50.

- Quite different than claiming the overall U.S. economy is in a recession. After all, protectionism hits manufacturers worse than most sectors. And historically the ISM Manufacturing needs to be in the vicinity of 43 before the broader economy itself is usually contracting.

- It should also be acknowledged that the less closely watched Markit U.S. Manufacturing PMI has just performed the opposite trick, rising from 49.9 to 50.3.

- In short, the drop in the ISM Manufacturing Index is bad news, consistent with a struggling economy, and indicative of a higher than usual recession risk. But we already knew much of this, particularly given that the New York Fed’s own yield curve recession model points to a recession risk in the 30% to 40% range for the coming 12 months.

Consumer bad news:

- We have generally celebrated the consumer as a source of resilience in the U.S. economy, supported by a robust personal savings rate, solid job creation, decent wage growth, limited household leverage and a high level of confidence.

- Alas, this last pillar is beginning to crumble. One of the two main consumer confidence metrics for the U.S. has just fallen quite sharply, arguing that the barrage of protectionist announcements and market volatility paired with slower growth is starting to undermine the engine of the U.S. economy.

- The University of Michigan Consumer Sentiment Index has just fallen by a whopping 8 points, from 98.4 in July to 89.8 in August. For context, this is not a horrible reading. But it is nevertheless the lowest figure since October 2016 and the biggest monthly decline since December 2012.

- There would appear to be a fair chance that the confidence metric falls further in September. September 1 marks the initiation of a 15% U.S. tariff on disproportionately consumer-oriented Chinese products. This is in contrast to prior rounds that had been focused more on intermediate goods and were thus less visible to American households.

- For the record, the other key metric of U.S. consumer confidence comes from the Conference Board. It did not fall as sharply in August, but is nevertheless also at its lowest reading since late 2016 by virtue of a steadier decline over the span of many months.

- Of course, while 2016 proved a challenging year in several regards, it did not ultimately culminate in recession. Nor must the latest trend result in the worst-case scenario. But the margin for error is shrinking.

Vetting the U.S. employment trend:

- In evaluating late-cycle economic conditions, the U.S. labour market warrants close attention.

- The rate of non-farm payroll job creation has slowed palpably over the past year, from a 6-month moving average of +236K as of July 2018 (even after recent downward benchmark revisions) to just a +141K average in July 2019.

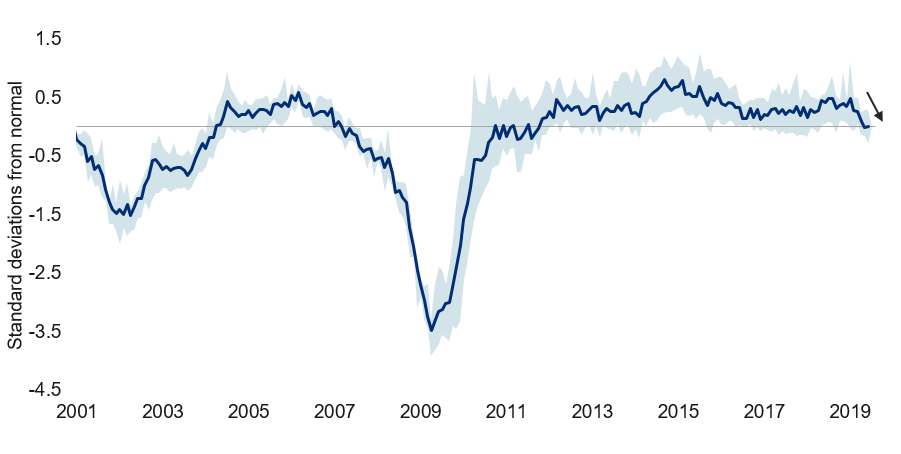

- Reflecting this in a broader sense, our U.S. labour market composite indicator has fallen from reliably positive territory over the past seven years to a zero reading today (see chart). chart

-

U.S. labour market momentum has faded

Note: As of Jun 2019. Normalized index of employment variables measuring rate of forward progress. Zero is historical average. Shading shows central tendency of indicators. Source: Haver Analytics, RBC GAM

- To be fair, a reading of zero in the indicator means that the index is at a perfectly normal level, though it is nevertheless also at its lowest reading in nearly eight years. Similarly, adding an average of 141K net new workers per month is, if anything, better than we should expect over the long run given the rate of working-age population growth.

- In short, there is nothing overly problematic in the job numbers, other than the fact that they aren’t sizzling like they used to.

- Traditionally, reversals in the trend unemployment rate and trend jobless claims are used as a gauge for identifying a turning point in the economic cycle. Today, these are no longer falling, which is concerning, though they also cannot be said to be rising. Both are bumping along the bottom, going roughly sideways. This is actually quite an unusual development. They usually keep falling (improving) until the day they start rising (deteriorating).

- The conclusion here is that the labour market is no longer actively strengthening. Nor is it weakening ominously. It needs to be watched very closely. The consensus is for an unobtrusive 160K employment gain in August – though one wonders if there is downside risk to the forecast given the recent drop in consumer confidence and a sub-50 employment sub-component in the ISM Manufacturing Index. September will then get quite blurry as downward hurricane distortions potentially interfere with the data.

Stall speed:

- After gory discussions about weakness in various parts of the U.S. economy, it is worth highlighting a silver lining: the stall speed of the U.S. (and, indeed, the global) economy has likely fallen.

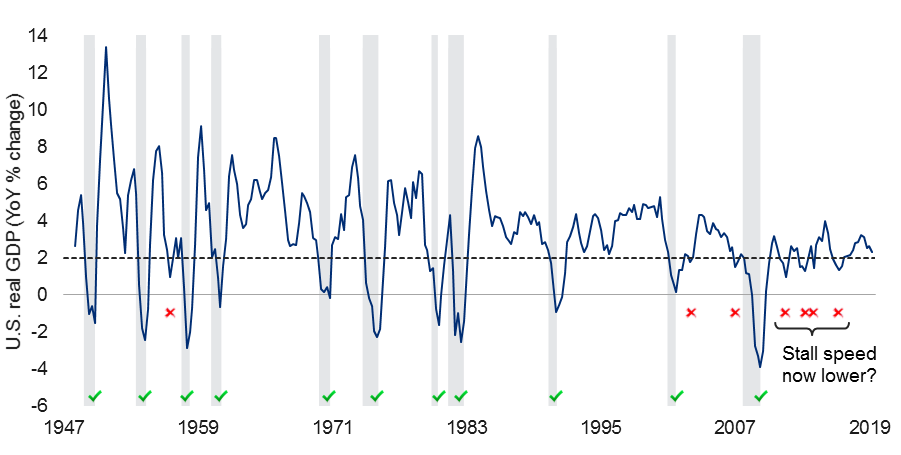

- Once upon a time, real U.S. GDP growth of below 2.0% year-over-year was a nearly sure-fire recipe for a recession, as demonstrated by the following chart.

-

Historical 2% stall speed now up for debate

Note: As of Q2 2019. Shaded area represents recession. Source: BEA, Macrobond, RBC GAM

- The idea is that when growth had fallen sufficiently far below normal, businesses and households reacted with such concern that a snowball effect of non-spending pushed the economy into outright recession.

- The good news is that the stall speed no longer appears to be 2.0%. A recession was avoided in six of the past seven such occasions.

- The question then becomes whether the concept of “stall speed” is no longer relevant, or instead if the stall speed has simply changed.

- Our vote is for the latter option. When economic actors become sufficiently concerned – whether justified or not – a mild slowdown can easily become worse. What might the stall speed be today? Given a lower economic speed limit today than in the past, we figure the U.S. stall speed is also proportionately lower, perhaps in the range of 1.0% today.

- The good news is that even as U.S. GDP growth slows, it is not yet anywhere near our hypothesized 1.0% threshold.

Other:

- Bank of Canada: The BoC proffers its next interest rate decision this Wednesday September 4th. No rate change is expected given the prior stance of the central bank, a recent robust GDP print and normal inflation readings. That said, the risk of a rate cut is non-zero given the following:

- The Bank’s demonstrated willingness to cut without notice

- The easing trend elsewhere

- Mounting protectionism

- Slowing global growth

- Looking further out, we continue to think the Bank of Canada will find its way toward rate cuts before too long. The market concurs with a 60% probability assigned for the bigger October meeting.

- Brexit: Brexit developments are arriving rapidly, likely making this commentary stale before the ink has dried. Nevertheless, the Conservative Party has now lost its working majority in parliament by virtue of an earlier by-election loss paired with the fresh defection of a Tory to the Liberal Democrats. A confidence vote could now pull down the government of Boris Johnson, triggering a change of government and very likely a new path for Brexit away from the no-deal hardline trajectory currently underway.

- However, despite now possessing the requisite numbers and a strong desire to avoid that Brexit scenario, there is a great reluctance among centrists to elevate Labour leader Jeremy Corbyn to the role of Prime Minister. If a confidence vote does not fail, parliament will adjourn next week and return barely two weeks before the October 31 Brexit deadline.